The Paper Substitute: Agency Mortgage-Backed Securities and the Next Saleability Crisis

In the previous essay in this larger series, I argued that the American single-family home scores at the bottom of Menger's saleability spectrum — illiquid, indivisible, non-transportable, non-homogeneous, and continuously encumbered by a perpetual ground rent payable to the state. By every measurable criterion that Menger's 1892 framework treats as fundamental, housing is among the least saleable major asset classes in the household's universe of options.

This conclusion poses an immediate puzzle. The U.S. mortgage market is approximately $14.5 trillion. Roughly $9 trillion of that is held in the form of agency mortgage-backed securities — paper claims issued by Fannie Mae, Freddie Mac, and Ginnie Mae against pools of underlying mortgages. These securities trade in the second-largest fixed-income market on earth, exceeded only by the U.S. Treasury market itself. They settle in seconds. They price continuously. They are accepted as collateral throughout the global financial system. The market for them is, by every conventional measure of liquidity, profoundly deep.

How can a profoundly liquid paper market exist on top of a profoundly illiquid underlying asset? The answer is the central observation of this essay, and it sits at the heart of what Antal Fekete spent his career warning about.

The agency MBS market is not, in Menger's sense, liquid. It is a deep market in paper substitutes for an underlying whose own saleability is permanent and structural. Under normal conditions, the substitute behaves as if it inherits the saleability properties of cash — because the federal guarantees, the open-market operations of the central bank, and the deep secondary-market infrastructure all collaborate to maintain that appearance. Under conditions of stress, the substitute's apparent saleability decays toward the saleability of the underlying. In 2008, the world saw the first sustained example of this decay in modern financial history. The mechanism that produced 2008 has not been reformed. It has been institutionalized, expanded, and folded directly into the Federal Reserve's primary balance sheet.

The next time it fails, the failure will be larger.

Fekete's framework, restated for the secondary mortgage market

Fekete's most consistent analytical move, across his entire body of work, was to insist that paper substitutes for a monetary or near-monetary good are reliable only to the degree that their redemption mechanics are real. A bank note redeemable in gold at sight is a near-perfect substitute for gold under conditions where the bank's solvency is unquestioned. The same note becomes a fractional claim — and ultimately, in Fekete's terminology, a broken substitute — once the redemption mechanism becomes uncertain. The transition from substitute-as-money to substitute-as-defaulted-claim is rarely gradual. It is a regime shift, often triggered by a specific event, that propagates rapidly through the population of holders once the regime has shifted.

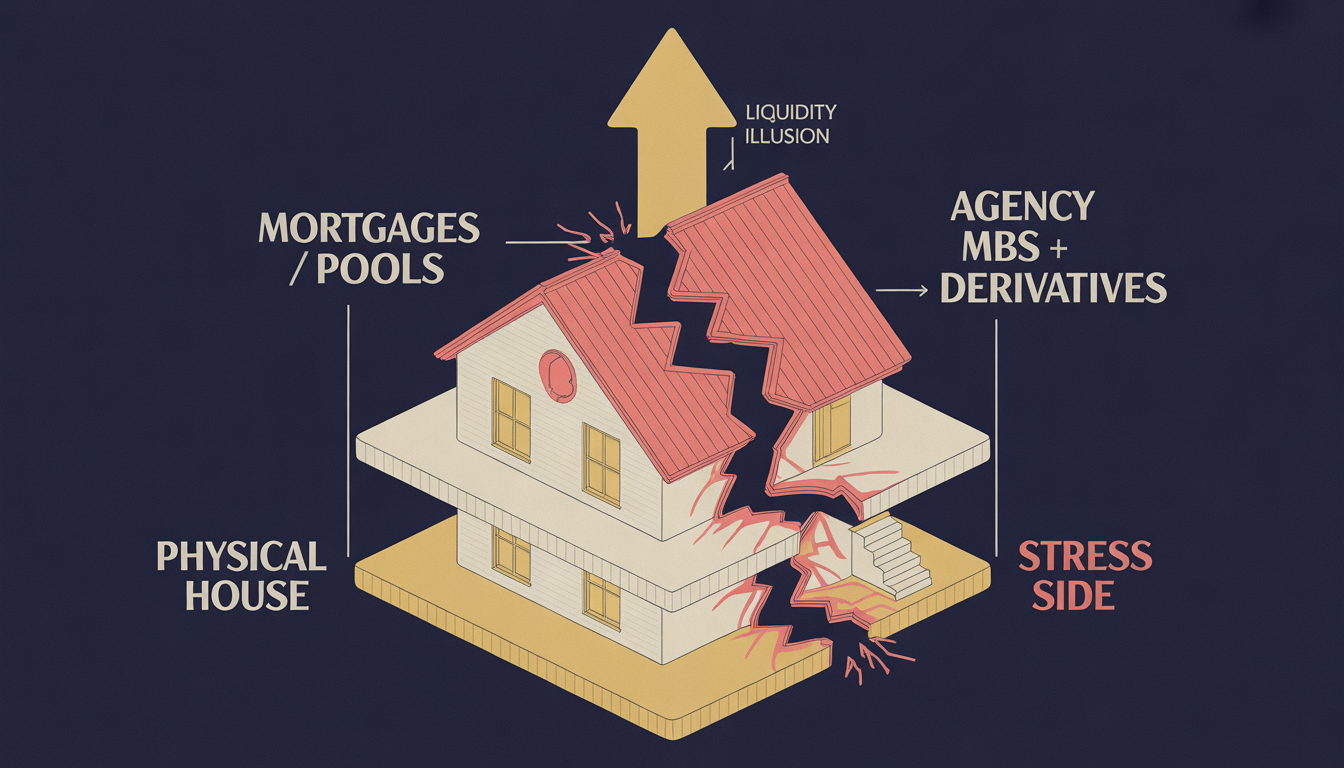

Fekete applied this analysis primarily to gold-backed currencies and to the gold basis. But the framework generalizes to any paper claim against any underlying. An agency MBS is a paper claim against a pool of mortgages, each of which is a claim against a household, which in turn is a claim against the home that secures the loan. The structure has three layers of paper before reaching the underlying physical asset:

Layer 1: the household's mortgage — a contractual claim against the household's future cash flows, secured by a lien on the home.

Layer 2: the agency MBS — a securitized claim on the cash flows from a pool of such mortgages, with federal credit enhancement attached.

Layer 3: derivatives on the agency MBS market — interest-rate swaps, options, structured products that reference MBS pricing or duration.

In normal market conditions, each layer trades as if it were nearly fungible with the next. The household's mortgage is sold to the agency at par. The agency-issued MBS trades at a tight spread to comparable Treasuries. The derivative book references MBS prices that are themselves continuously determined by deep cash-market activity. Apparent saleability flows up the stack, from the federal guarantee at the top, through the agency wrapper, through the secondary-market infrastructure, all the way down to the original mortgage. The household, the bank, the agency, and the bondholder all behave as if the chain is solid.

Under stress, the chain reveals itself for what it is: a series of distinct, structurally-imperfect substitutions, each of which can fail independently. This is the Fekete observation. The depth of the secondary-market infrastructure does not eliminate the substitutability problem. It conceals it under normal conditions and amplifies it under stress, because participants who have been treating the chain as solid are forced to discover, often simultaneously, that they have been holding paper substitutes whose redemption mechanics are not what they assumed.

What 2008 actually was

The 2008 financial crisis is conventionally narrated as a story of subprime lending excess, regulatory failure, and the collapse of specific firms. This narrative is not wrong, but it misses the deeper structural event. What collapsed in 2008 was the substitute layer of the American mortgage market.

The proximate trigger was a wave of defaults in the subprime mortgage segment. The proximate damage was concentrated in the private-label MBS market — securities issued by investment banks rather than by the federal agencies. But the deeper signal was the brief and partial spread blowout in the agency MBS market itself. Agency MBS, which had traded for decades at a tight spread to Treasuries on the assumption that federal credit enhancement made the spread irrelevant, briefly traded at distressed levels in the panic phase of 2008. The Federal Reserve's response — beginning with the November 2008 announcement of $500 billion in agency MBS purchases, which expanded by January 2009 into the first formal quantitative easing program — was a direct intervention to prevent the agency MBS market from discovering its own substitute-layer fragility.

The intervention worked. Spreads compressed. The market stabilized. The agencies were placed into federal conservatorship in September 2008, formalizing the implicit federal guarantee as an explicit one. The lesson the policy establishment took was that the system had been saved by aggressive central-bank action and direct federal support.

The lesson the policy establishment did not take — and that the New Austrian framework would have insisted on — is that the substitute structure itself was the problem. The 2008 episode demonstrated that under sufficient stress, the agency MBS market could decouple from its underlying fundamentals in ways that conventional risk models did not predict. The "fix" was to remove the question entirely by having the central bank become the marginal buyer of agency MBS in any future crisis, and by formalizing the federal backstop. This did not fix the substitute structure. It merely ensured that any future failure would have to be larger, more systemic, and more expensive to paper over than the 2008 failure was.

Where the agency MBS market sits in 2026

The current configuration of the agency MBS market, eighteen years after the conservatorship of Fannie and Freddie, is more concentrated, more central-bank-dependent, and more structurally fragile than it was in 2007.

Total agency MBS outstanding: approximately $9 trillion.

Federal Reserve holdings of agency MBS: approximately $2.2 trillion as of early 2026, down from a peak of $2.7 trillion in 2022 but still vastly larger than at any pre-2008 baseline.

Share of new issuance absorbed by the Fed during peak QE periods: approached 100%. In multiple months between 2020 and 2022, the Federal Reserve was the only net buyer of new agency MBS, with all private demand absorbed by Fed purchases.

Conservatorship status of Fannie Mae and Freddie Mac: ongoing, eighteen years after the original "temporary" intervention. Multiple administrations have proposed plans to release the agencies from conservatorship; none has succeeded. The implicit guarantee is now indistinguishable from an explicit guarantee for all practical market purposes.

Mortgage origination market share by entity type: nonbanks now originate roughly 70% of all new U.S. mortgages, up from approximately 30% in 2007. The bulk of these nonbank originations are sold immediately into agency MBS pools, with the originator retaining no skin in the game beyond the servicing rights.

Concentration in long-duration paper: the post-2020 vintage of agency MBS is concentrated in coupons of 2.5–3.5%, against a current market rate of 6.23%. These securities are deeply underwater on a mark-to-market basis. The Federal Reserve's $2.2 trillion holdings are estimated to carry unrealized losses in the hundreds of billions, which the Fed reports through its remittances-to-Treasury accounting but does not realize as a balance-sheet event.

This configuration is not a neutral structure that happens to support housing finance. It is a system in which the largest fixed-income market in the world after Treasuries is supported by a central bank that has effectively committed to backstop it permanently, against an underlying asset class whose Mengerian saleability is permanently low. The system is "stable" in the sense that the central-bank backstop has so far always proven sufficient. It is fragile in the deeper sense that the backstop is itself a substitute for the saleability properties the underlying does not have.

The mechanism by which the next failure happens

The framework predicts a specific shape for the next agency MBS crisis. The shape is not a 2008-style cascading default in the underlying mortgages. The credit enhancement around the agencies is now explicit and federally guaranteed; mortgage default does not transmit to MBS holders the way it did in 2008. The framework predicts something subtler and arguably more dangerous.

The next failure will be a duration crisis in the substitute layer.

The mechanism is straightforward. The agency MBS market currently carries an enormous embedded short on rising long-term rates. Holders of low-coupon MBS issued during the 2020–2022 ZIRP era are exposed to substantial mark-to-market losses if long rates rise materially. The Federal Reserve itself is the largest holder of this paper, with the consequences absorbed through quasi-fiscal accounting that obscures the loss without eliminating it. Banks holding agency MBS for regulatory capital purposes faced the first wave of this exposure in 2022–2023, contributing directly to the SVB and First Republic failures discussed elsewhere in this series.

If long rates were to rise sharply — driven by, for example, sustained inflation from the Iran war energy disruption, a credit downgrade of U.S. Treasuries, a foreign reserves rotation away from dollar-denominated assets, or any combination of these — the mark-to-market losses on the agency MBS market would become an order of magnitude larger than what the 2022–2023 episode produced. The Federal Reserve's response toolkit is constrained: it cannot lower rates without re-igniting the inflation it is trying to contain, it cannot sell its MBS holdings without realizing the losses it has been absorbing through accounting, and it cannot expand its balance sheet without compounding the duration mismatch.

The most likely policy response under such conditions is a yield curve control regime — direct central-bank action to cap long-term rates regardless of market preference. This is the trajectory Japan has been on since 2016. It works arithmetically: if the central bank commits to buying unlimited quantities of bonds at a target yield, the target holds. But it works through the same mechanism Fekete identified as the most corrosive: the central bank prevents the market from discovering its own equilibrium, which means the substitute structure continues to exist while its substitute-ness continues to grow more extreme. The price stability is purchased at the cost of further saleability decay in the underlying claims.

Under yield-curve control, the agency MBS market would technically continue to function. Spreads would remain compressed by central-bank backstop. Trading activity would continue. But the Mengerian saleability of the paper would have crossed a threshold from "deep substitute for cash" to "explicitly central-bank-supported asset whose price reflects policy commitment rather than market demand." The decay function from the third essay in this series predicts that under such conditions, the marketability spreads in adjacent markets — gold basis, FX basis, repo dispersion — would widen even as the agency MBS market itself appeared calm. The failure would be visible everywhere except in the market that had been the source of it.

Why this is the housing-trilogy problem

The relevance of this analysis to housing as a household decision is direct, even though the household never interacts with the agency MBS market explicitly. Three structural consequences flow from the configuration described above.

First, the household's mortgage is priced by a market that depends on continued central-bank intervention to function. When you borrow at 6.23% in 2026, the rate you pay is not a market-clearing equilibrium between household credit demand and private investor supply of capital. It is the rate that emerges from a market structure in which the Federal Reserve has held $2 trillion-plus of agency MBS for six years, in which the agencies themselves are in eighteenth-year conservatorship, and in which roughly half of all mortgage originations flow through nonbank originators with no balance-sheet capacity to hold the loans they make. The "market" rate is a policy artifact. The household-as-bond-issuer described in the previous essay is issuing bonds into a market that requires continuous central-bank support to absorb them.

Second, the household's mortgage is exposed to the agency MBS market's structural fragility through a back channel: refinancing access. A homeowner with a 6.23% mortgage in 2026 carries an implicit option to refinance if rates fall. The value of that option depends entirely on the continued functioning of the agency MBS market — which is the secondary market through which any refinanced loan must clear in order for the originator to recoup capital. If a duration crisis in agency MBS causes that market to seize up, refinance windows close regardless of where headline rates trade. Households who anticipated being able to refinance discover that the channel has narrowed or temporarily closed. The optionality embedded in the fixed-rate mortgage degrades silently with the saleability of the substitute layer above it.

Third, the broader behavioral case for buying — that home prices have appreciated reliably for nine decades — is in part a consequence of the substitute structure rather than of housing's intrinsic productive value. The 30-year mortgage architecture, the agency MBS secondary market, and the central-bank backstop together create a continuous financing supply for housing that is structurally larger than what an unsupported private market would generate. More financing supply produces higher home prices over time, particularly in supply-constrained markets. A material portion of the historical home-price appreciation that homeowners attribute to the merits of housing as an investment is in fact the propagation of the financing-supply expansion through the demand side of the housing market. If the substitute structure ever fails — even partially, even temporarily — the financing-supply expansion reverses, and home prices respond accordingly.

These three consequences are not predictions about a specific date or a specific crisis. They are statements about the structure of the household's exposure. Owning a home in 2026 is owning an asset whose financing market is permanently dependent on central-bank intervention, whose embedded refinance option depends on that market's continued functioning, and whose long-run appreciation has been substantially driven by the same architecture's forty-year expansion. When the architecture's saleability decays — and the decay is observable in the proxies described in essay three of this series — the household's exposure decays with it.

What an honest analysis of agency MBS would conclude

A neutral analyst, applying the framework rigorously, would reach four conclusions about agency MBS in 2026 that the conventional financial press does not.

First, agency MBS is not a fixed-income asset class in the same sense as Treasuries. It is a derivative position, two paper layers removed from a structurally illiquid underlying, whose continued functioning depends on permanent central-bank support. Treating it as a near-equivalent to Treasuries — as nearly every institutional fixed-income manager does — is a category error.

Second, the Federal Reserve's $2.2 trillion in MBS holdings is not "balance sheet" in the conventional sense. It is a quasi-fiscal commitment to maintain the substitute layer that makes American household housing finance functional. Reducing the holdings is constrained by the political economy consequences of letting the substitute layer's true saleability emerge in market prices. The Fed will continue holding most of these securities indefinitely, regardless of what its formal balance-sheet runoff guidance says.

Third, the next crisis in the agency MBS market will be a duration crisis, not a credit crisis, and the policy response will be yield-curve control or its functional equivalent. This is the trajectory Japan has been on since 2016 and that the European Central Bank flirted with during the eurozone debt crisis. The framework predicts the United States will follow the same path under sufficient stress, because no other tool in the central-bank toolkit can address the duration mismatch without realizing the losses that the policy establishment has spent two decades concealing.

Fourth, household homeownership as a financial decision is more exposed to this structure than the conventional analysis recognizes. The household pays the mortgage rate that the substitute market produces. The household's home-price appreciation reflects the financing-supply expansion the substitute market enables. The household's refinance optionality depends on the substitute market's continued functioning. A meaningful fraction of household financial planning over the past several decades has been an unwitting bet on the continued integrity of an architecture that the New Austrian framework identifies as structurally fragile.

The Mengerian endnote

Menger's framework is unsparing on the question of what happens when a substitute layer becomes structurally separated from its underlying. Either the substitute remains tethered through real redemption mechanics — at which point its saleability genuinely tracks the underlying's — or the substitute drifts free, supported by institutional commitments rather than by redemption discipline, and accumulates a saleability premium that exists only as long as those commitments hold. The premium is not a stable feature. It is a regime, and like all regimes, it persists until the conditions that produced it shift.

The agency MBS market has been operating in the second mode for eighteen years. The conditions that produced the regime — explicit federal credit enhancement, central-bank balance-sheet absorption, conservatorship of the issuers, and the broader framework of post-2008 financial repression — are not permanent features of the political economy. They are policy choices, made by specific people in specific institutional positions, and they can be unmade by the same kinds of choices in the future. The framework does not predict when. It predicts that when the unmaking happens, the saleability of the substitute layer will revert toward the saleability of the underlying, and the underlying — as the previous essay documented — sits near the bottom of Menger's spectrum.

The household holding a 6.23% mortgage in 2026 is, in the most literal sense, a counterparty to the substitute layer. The household issued the bond. The agency wrapped the bond. The Federal Reserve absorbed a large share of the wrapped paper. The structure's stability is the household's stability. When the structure's saleability decays, the household's position decays with it.

Fekete spent his career arguing that the only honest path through monetary instability runs through redemption discipline — through claims whose substitute relationships to underlyings are real and verifiable, not maintained by institutional commitment. The agency MBS market is the largest counter-example to this principle in modern finance. Eighteen years of post-2008 institutional repair have made it more central to the American financial system, not less. When the next saleability crisis arrives — and the framework treats this as a question of timing rather than of possibility — the agency MBS market will be at or near its center.

The homeowner who has read this far has the right framework to evaluate what that means for their own position. The conventional financial press will not provide that framework. It does not have the vocabulary. The New Austrian Economics does. The next essay in this trilogy turns from the structural critique to the empirical one — to the specific cohort of Americans who captured a one-time monetary windfall during the substitute layer's expansion phase, and the cohort that is now being asked to pay them out at terms that the underlying economic reality cannot sustain.

This is the first essay of the Housing Trilogy within the New Austrian Economics series. The trilogy applies the Menger-Fekete framework specifically to the American household's most consequential financial decision and to the architecture surrounding it. Subsequent essays will examine the intergenerational arbitrage embedded in the post-1971 housing market and propose what an honest replacement for the 30-year mortgage architecture would look like under a sound monetary regime.