Canberra had given me the diagnostic — the gold basis as monetary thermometer, the direction of travel toward permanent backwardation. Auckland, two years later, gave me the architecture — what a sound monetary system actually looks like, how it works, what specifically makes it break down, and what the path back might be.

Professor Antal Fekete returned to New Zealand in late 2011 with Sandeep Jaitly, Rudy Fritsch, and Keith Weiner for a week-long symposium titled Gold and Economic Freedom, hosted at the University of Auckland Business School by Louis Boulanger. It was the second Auckland event in the series — the first had run in November 2010 under the title Sound Money or Unsound — That is the Question — and the ideas had deepened considerably in the intervening year.

The Spread as the Key to Economic Understanding

Fekete opened the 2011 symposium with a lecture on the coordination of social interaction, and he began — as he often did — with Carl Menger. "Carl Menger is universally successful in all he touched," he said. "In balance, Aristotle comes out pretty average."

The claim was made in seriousness. Menger's fundamental insight — that economic value is subjective, that prices arise not from intrinsic worth but from the bidding and offering of individuals acting on their own assessments — is familiar enough. What is less often noted is that Menger's deeper contribution was not the price but the spread: the difference between the price at which you can buy and the price at which you can sell. At any given place and time, there are at least two prices for the same good. The gap between them is not noise; it is signal. It tells you something about the degree to which a good is saleable — how easily it can be converted into the specific thing you actually want.

This is Menger's theory of Absatzfähigkeit, saleability or marketability, and it is the foundation on which everything else in the New Austrian framework rests. The most saleable good — the one with the narrowest spread, the one you can sell to the most people on the most favorable terms — becomes money.

Social coordination, Fekete continued, is a cobweb. Any disturbance at one node sends vibrations through the entire system. Maladjustments keep occurring as adjustments are made; the economy is never in equilibrium, only approaching it asymptotically. What makes a sound monetary system sound is not that it eliminates disturbances — it cannot — but that it provides a medium through which the cobweb can absorb and redistribute shocks rather than amplifying them.

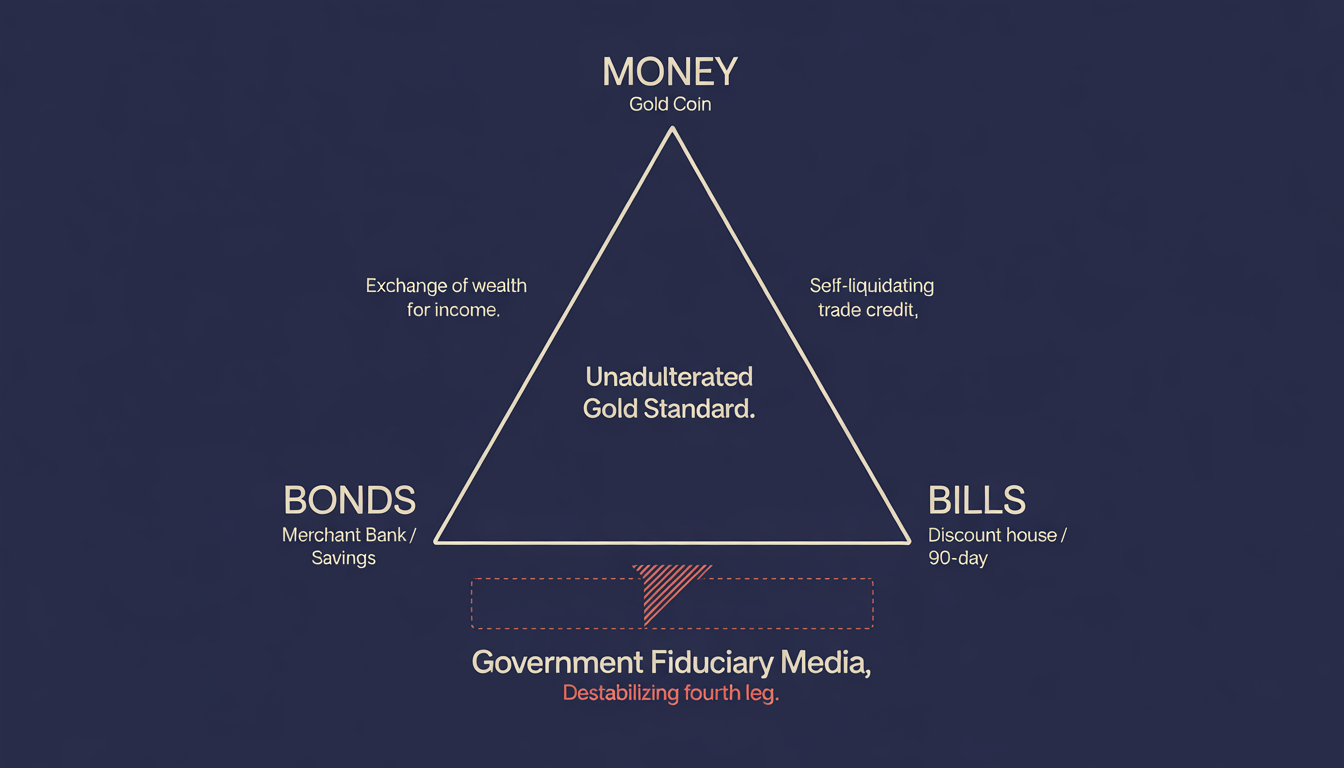

The Three-Legged Gold Standard

The most memorable visual from the entire Auckland series came from Rudy Fritsch in the 2011 symposium's afternoon sessions: a deceptively simple triangle, three vertices, three connecting sides, labeled at each corner with one word.

Money. Bonds. Bills.

The triangle encodes an entire theory of credit.

Money — at the apex — is gold coin. It is that which extinguishes all debt. It is not wealth; wealth is productive capacity. Money is the medium through which wealth is stored and transferred. Legal tender laws attempt to equate paper with gold, present goods with future promises. They cannot do so permanently; they merely defer the reckoning.

Bonds — dealt in by merchant banks — represent savings-based credit. An old man has accumulated wealth over a productive life. A young man has productive capacity but lacks capital. The bond market mediates the exchange: wealth today for income tomorrow, with interest as the measure of the efficiency of that exchange over the alternative of hoarding. The interest rate is not, as Mises argued, a reflection of time preference — the inherent human preference for present over future gratification. It is, in Fekete's formulation, the measure of the marginal efficiency of exchanging accumulated wealth for a future income stream, relative to the option of simply hoarding.

Bills — dealt in by discount houses — represent consumption-based credit. A wholesaler has goods ready for market; a retailer can sell them within ninety days but cannot pay cash today. The real bill bridges that gap. It circulates, endorsed from hand to hand, as the clearing medium of commerce. It is self-liquidating: when the goods reach the consumer and are paid for, the bill is extinguished. No new money is created; existing productive capacity is simply mobilized more efficiently.

The triangle is stable because the three elements constrain and balance each other. Add a fourth leg — government fiduciary media, paper issued without gold backing and not arising from any productive transaction — and you destroy the triangle's geometry. You introduce an element that is neither self-liquidating nor constrained by the discipline of the gold market.

Illicit Interest Arbitrage and the Inverted Yield Curve

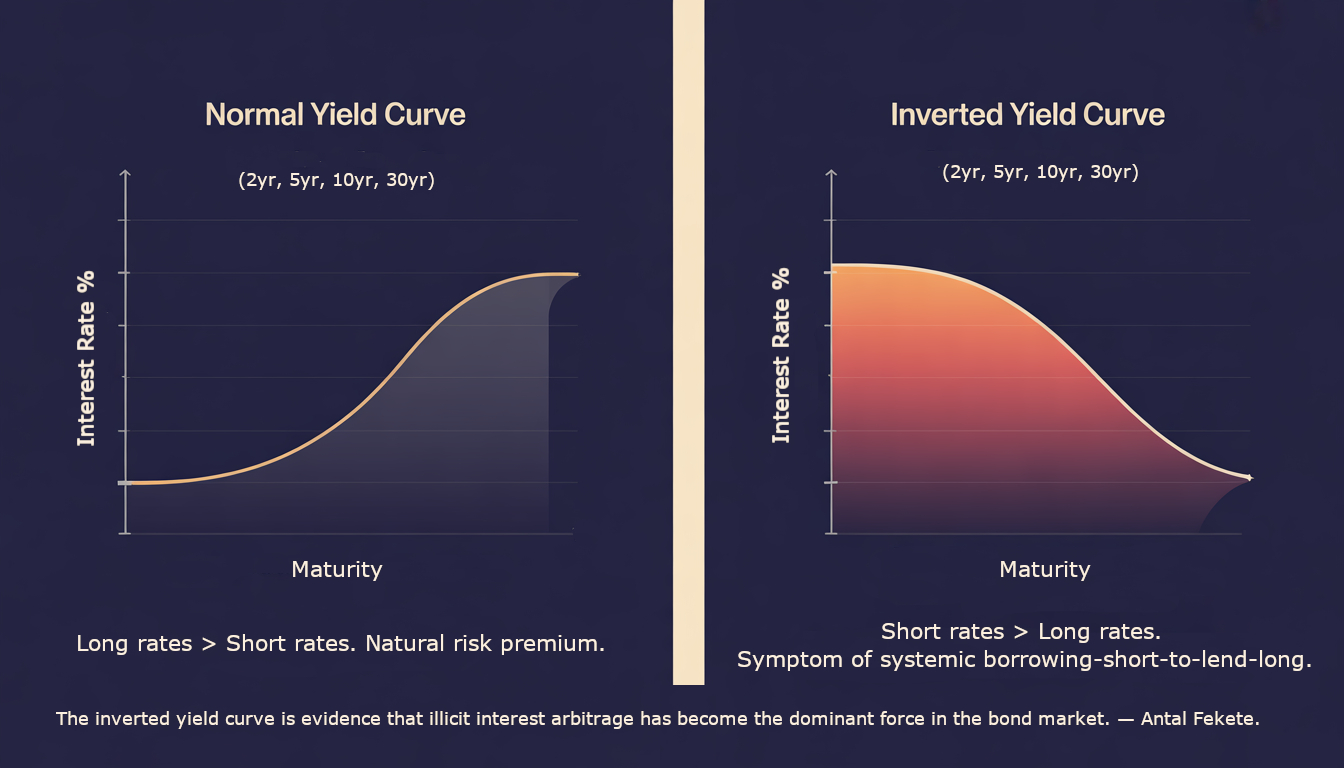

In the 2010 symposium and again in 2011, Fekete returned repeatedly to the concept of illicit interest arbitrage — the practice of borrowing short to lend long. It is the defining pathology of the adulterated monetary system, and understanding it requires first understanding why the yield curve normally slopes upward.

Under a sound monetary system, interest rates rise with the term of the loan. A one-year loan commands a lower rate than a ten-year loan; a ten-year loan commands a lower rate than a thirty-year loan. The reason is intuitive: longer commitments expose the lender to greater uncertainty. The future is unknowable, and risk accumulates with time. This is the normal yield curve.

Now introduce the possibility of risk-free profit through arbitrage. If the thirty-year bond yields more than the ten-year, an institution can profit by buying the thirty-year and selling the ten-year short. The spread is the profit — or would be, except that the short position matures before the long one, and interest rates may change in between. This is not risk-free. It is a bet on the interest rate staying stable or falling. In a normal market, such bets sometimes win and sometimes lose, and the discipline of losses keeps the practice bounded.

But when the Federal Reserve enters the picture — announcing in advance the dates and quantities of bonds it will purchase — the game changes. Bond speculators can preempt Fed purchases, buying the targeted securities before the Fed bids for them and selling at a guaranteed profit. The risk has been removed. The profit is not a return for bearing uncertainty; it is a transfer from the monetary system to the privileged institutions (the primary dealers — Goldman Sachs, JP Morgan, and a handful of others) that enjoy advance knowledge of Fed intentions.

The consequences compound over time. More and more capital migrates toward this risk-free trade. More and more institutional balance sheets become leveraged long in long-duration bonds financed by short-duration borrowing. When short rates are forced to zero — as they were after 2008 — the thirty-year bond becomes the target, and the game extends further out the curve. The entire yield curve is progressively flattened and eventually inverted, producing the paradoxical situation where shorter-term money commands a higher rate than longer-term money.

The inverted yield curve is not merely an economic curiosity. It is, Fekete argued, conclusive evidence that borrowing short to lend long has become so widespread that its collective effect on the market exceeds the natural forces that would make long rates higher than short rates. The inversion is the system telegraphing its own instability.

"Illicit interest arbitrage has to be outlawed. This is the most important single feature of the unadulterated gold standard — not what it contains, but what it prohibits."

Hoarding and the Interest Rate

One of Fekete's most original contributions — and the one that most clearly distinguishes the New Austrian framework from Misesian orthodoxy — concerns hoarding and its role in regulating the interest rate.

In the mainstream view, and in Mises's own framework, hoarding is treated as a kind of withdrawal from economic circulation — liquidity preference raised to a pathological extreme. In Fekete's view, hoarding is a rational, stabilizing mechanism that only gold can provide.

The argument: if the market interest rate rises above the equilibrium rate — the rate at which the exchange of wealth for income is equally attractive as holding gold — people will dishoard gold. Gold flows from hoards into the bond market. The increase in the supply of loanable funds puts downward pressure on the interest rate, moving it back toward equilibrium. Conversely, if the interest rate falls below the equilibrium rate, people hoard gold rather than lending it. The reduction in the supply of loanable funds puts upward pressure on rates.

This arbitrage between the gold hoard and the bond market is the mechanism by which a gold coin standard self-regulates the interest rate. Under a gold coin standard, hoarding removes bank reserves and forces a contraction of credit — precisely the feedback loop needed to prevent rates from being driven to zero and held there artificially. Remove gold from the system, and the feedback loop is severed. Interest rates become a policy variable rather than a market outcome, and the consequences — including everything documented in the Canberra lectures on capital destruction — follow necessarily.

Gold Bonds to the Rescue

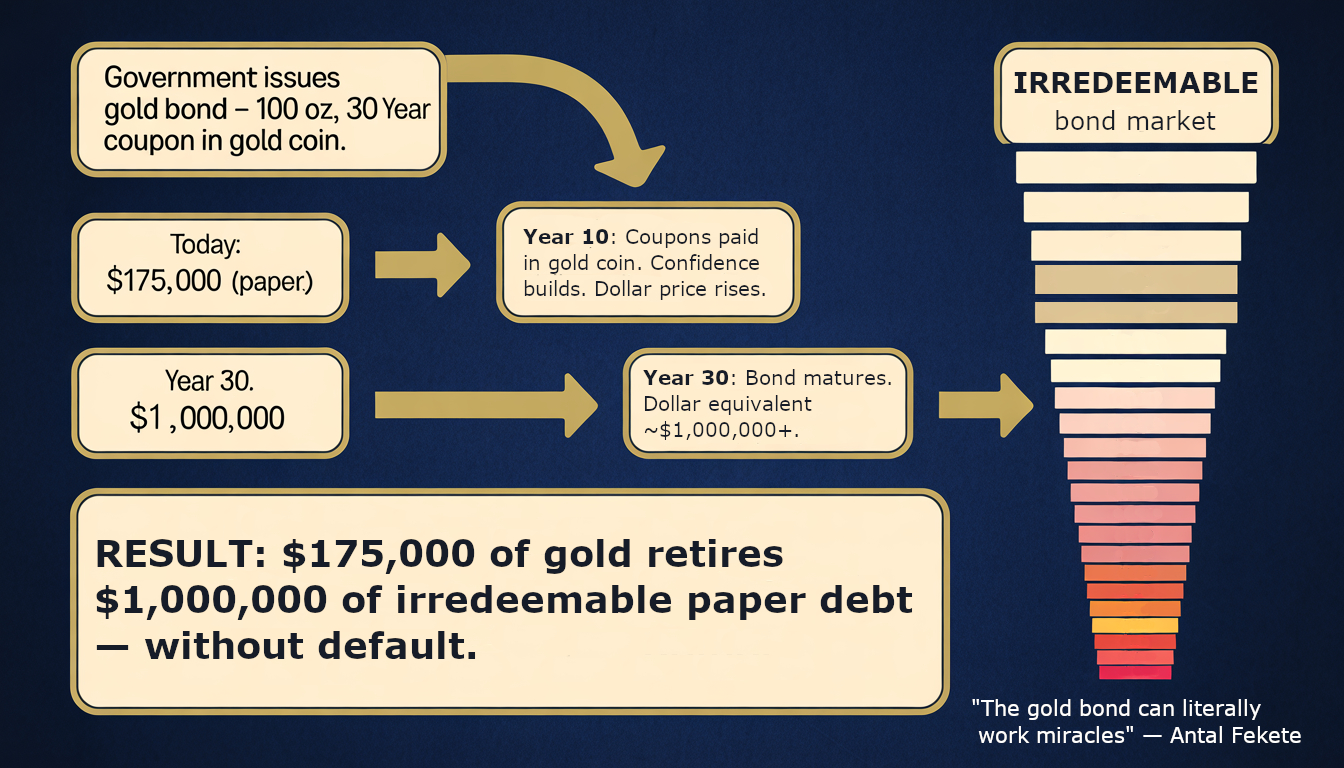

The 2011 symposium's most forward-looking material came in Fekete's lectures on gold bonds — a specific mechanism by which the current debt structure could theoretically be unwound without either hyperinflation or a deflationary collapse.

The mechanism is elegant. Suppose a government issues a one-hundred-ounce gold bond with a thirty-year maturity, paying coupon interest in gold coin. In today's dollars, such a bond might trade at $175,000. But as confidence in the issuing government's ability and willingness to pay in gold accumulates — as the coupons actually arrive in gold coin, year after year — the dollar price of the bond rises. By year thirty, the same bond might command a dollar price of $1,000,000 or more. The government has, in effect, borrowed $175,000 in today's dollars and — by maintaining its gold obligations — retired $1,000,000 in paper debt with the same amount of gold.

Gold bonds, on this argument, can extend the maturity of the debt structure (reversing the current trend toward shorter and shorter maturities as irredeemable debt loses credibility) and can retire irredeemable paper bonds without default. The prerequisite is opening the mint to free, unlimited gold coinage — ensuring that sufficient gold coin circulates to make the coupons credible.

Fekete noted that Thomas Jefferson's warning — "the banks and corporations will deprive the people of all property until their children wake up homeless on the continent their fathers conquered" — was not metaphor. It was a description of the precise mechanism by which risk-free bond speculation, enabled by central bank open-market operations, transfers wealth from the productive economy to the financial system. Gold bonds, by reintroducing a hard constraint on government borrowing, are the specific antidote.

Gold Ownership and the Physical Value Chain

Louis Boulanger closed the 2011 symposium with a practical lecture on gold ownership — the gap between what people believe they own and what they actually own.

The key distinction: allocated versus unallocated gold storage. An allocated account holds specific, identified bars of gold in your name. The institution storing them cannot lend them, lease them, or use them as collateral. You are a bailor; they are a bailee. An unallocated account, by contrast, makes you an unsecured creditor of the institution. The "gold" on your account statement is a liability of the bank, not a specific physical asset. In a crisis, unallocated gold holders discover that their gold — like London Metal Exchange claims — is the last in line behind depositors, bondholders, and whatever other creditors the institution has accumulated.

Gold ETFs, Boulanger noted, hold assets that have been borrowed from banks — making ETF holders several steps removed from physical metal. The irony: instruments designed to make gold ownership easier make it, in moments of stress, functionally non-existent.

His closing observation has stayed with me: "Bullion is hated by investment professionals because it does not require management skill." The entire apparatus of the financial industry — the fees, the management structures, the trading operations, the ETF wrappers — exists in part because physical gold in a vault under your direct control requires none of it.

The Arc from Canberra to Auckland

Leaving Auckland in 2011, I had something I had not had entering Canberra in 2009: a complete framework. Not merely a diagnosis of what was wrong — the vanishing basis, the approaching permanent backwardation — but a theory of what right would look like, why the twentieth century's attempts at gold standards had failed, and what the specific features of an unadulterated system would need to include.

The framework can be stated simply, though its implications are not simple at all:

A sound monetary system requires:

- Gold coin as money, freely minted and freely circulating

- Real Bills as the clearing mechanism of commerce, self-liquidating and arising naturally from productive transactions

- A bond market constrained by the discipline of gold, where merchant banks intermediate the exchange of savings for income

- The explicit prohibition of illicit interest arbitrage — borrowing short to lend long

- No fiduciary media issued by government without gold backing

The twentieth century eliminated each of these features, one by one, beginning with the elimination of Real Bills in 1914–1918 and ending with the closure of the gold window in 1971. The present system — fiat currencies, zero interest rates, derivatives towers, risk-free bond speculation, permanent QE — is not an alternative monetary architecture. It is the consequence of the methodical dismantlement of the original one.

What replaces it is the open question. Fekete believed the market, not governments, would eventually force the answer. The gold basis, declining since 1971, is still measuring the approach.

Notes from the Canberra 2009 conference are collected in The Vanishing Gold Basis: Field Notes from Canberra, 2009.

Related essays

The Vanishing Gold Basis: Field Notes from Canberra, 2009

Four days with Antal Fekete and the Gold Standard Institute in Canberra, eighteen months after Lehman. The gold basis as monetary thermometer, the mechanics of permanent backwardation, and why falling interest rates destroy capital in ways that no one in the financial press was discussing.

The Golden Triangle: Coin, Bills, Bonds, and the Operational Architecture of a Sound Monetary System

Most modern advocacy for the gold standard describes a monetary regime that is not, and has never been, the gold standard. The picture sketched in libertarian pamphlets and Austrian-tradition advocacy typically consists of paper currency backed by gold reserves held in a vault, with citizens nominally able to redeem notes for gold but rarely doing so. This is not the gold standard. This is the gold-exchange standard, a substitute system constructed at the 1922 Genoa Conference to replace the actual gold standard that the First World War had destroyed in 1914. The actual gold standard — the system that produced approximately a century of price stability, productive investment, and broadly distributed prosperity from the Napoleonic settlement through August 1914 — was a three-pillar operational architecture: gold coin in actual circulation, gold bills clearing short-term commercial transactions, and gold bonds providing the long-term capital and debt-retirement mechanism. Antal Fekete, drawing on Adam Smith's Real Bills Doctrine and Carl Menger's saleability framework, called this architecture the Golden Triangle. His student Rudy Fritsch and others in the New Austrian School have elaborated it. This essay engages the architecture in full: what each pillar was, how the pillars operated together, why the system was destroyed across the 1914-1971 period, and what its restoration would require. The Golden Triangle is not a nostalgic gesture toward a lost monetary regime. It is the operational expression of the saleability framework this catalog has been building from Article 1 forward — and it is the structural alternative to the substitute-layer architecture the catalog's prior thirty-two essays have documented across multiple sectors of contemporary economic life.

AI Compute as Nascent Real Bills: A Clearing Instrument for the Machine Economy

Fekete's most misunderstood idea — the Real Bills Doctrine — described how the 18th-century commercial economy spontaneously developed a short-duration, self-liquidating clearing instrument for goods in transit to the consumer. The 21st-century compute economy is developing the same thing, and no one is calling it what it is.