In November 2009, eighteen months after the collapse of Lehman Brothers and roughly a year into the most aggressive monetary expansion in Federal Reserve history, a small group of perhaps forty people gathered at University House on the grounds of the Australian National University in Canberra. They had come to hear Antal Fekete.

Gold was trading at around $1,100 per ounce. Quantitative easing had become a household term. The financial press was consumed with green shoots and exit strategies. None of that was what the Gold Standard Institute's conference — titled The Vanishing Gold Basis and the World Financial Crisis — was about. What it was about was something quieter, more structural, and in retrospect far more predictive: a number that almost no one in the financial world was watching, called the gold basis, that had been declining for thirty-five years and was now approaching zero.

A Preliminary Day: Gold Investment Day

The formal conference was preceded by a Sunday gathering bringing together speakers from the Australian investment world. David Evans of Sciencespeak.com made the provocative argument that carbon credits were simply a new form of fiat money — an artificially scarce permit system that would enrich the same financial institutions already profiting from monetary expansion. Barry Dawes of Global Speculator offered a long-view on resource sector positioning, noting that twenty-eight years of falling interest rates were nearing a trend reversal. Bron Suchecki of the Perth Mint provided a technical overview of the London bullion market's physical value chain and the mechanics of gold leasing — the practice by which gold earns its own interest rate, called the lease rate, and the way in which London bullion bank claims to gold change hands without the metal itself moving.

These were useful introductions. But the conference proper, beginning Monday, was where the intellectual framework began to take shape.

Day One: The Real Bills Doctrine and the Meaning of the Basis

Fekete opened the conference with remarks that established the conceptual ground everything else would build on. Two ideas dominated: Real Bills, and the gold basis.

Real Bills — commonly known today as invoices or commercial paper — are self-liquidating credit instruments that arise naturally in a gold standard economy. A wholesaler delivers goods to a retailer; the retailer cannot pay in gold on the spot but will be able to once those goods are sold, typically within ninety days. The bill represents that promise. It circulates among merchants, refiners, and wholesalers — bypassing the banking system entirely — and extinguishes itself when the goods reach the consumer and payment is made. The critical point Fekete emphasized: Real Bills are the clearing system of the gold standard. A gold standard without Real Bills is, in his phrase, a castrated gold standard — rigid where it should be elastic, unable to accommodate seasonal and cyclical swings in trade volume.

The present financial crisis, he argued, began not in 2008 but much earlier — in 1944, at Bretton Woods, when the multilateral clearing system that had made pre-World War I trade so efficient was dismantled. The 1971 closing of the gold window was simply the delayed consequence of that dismantlement, finally playing out.

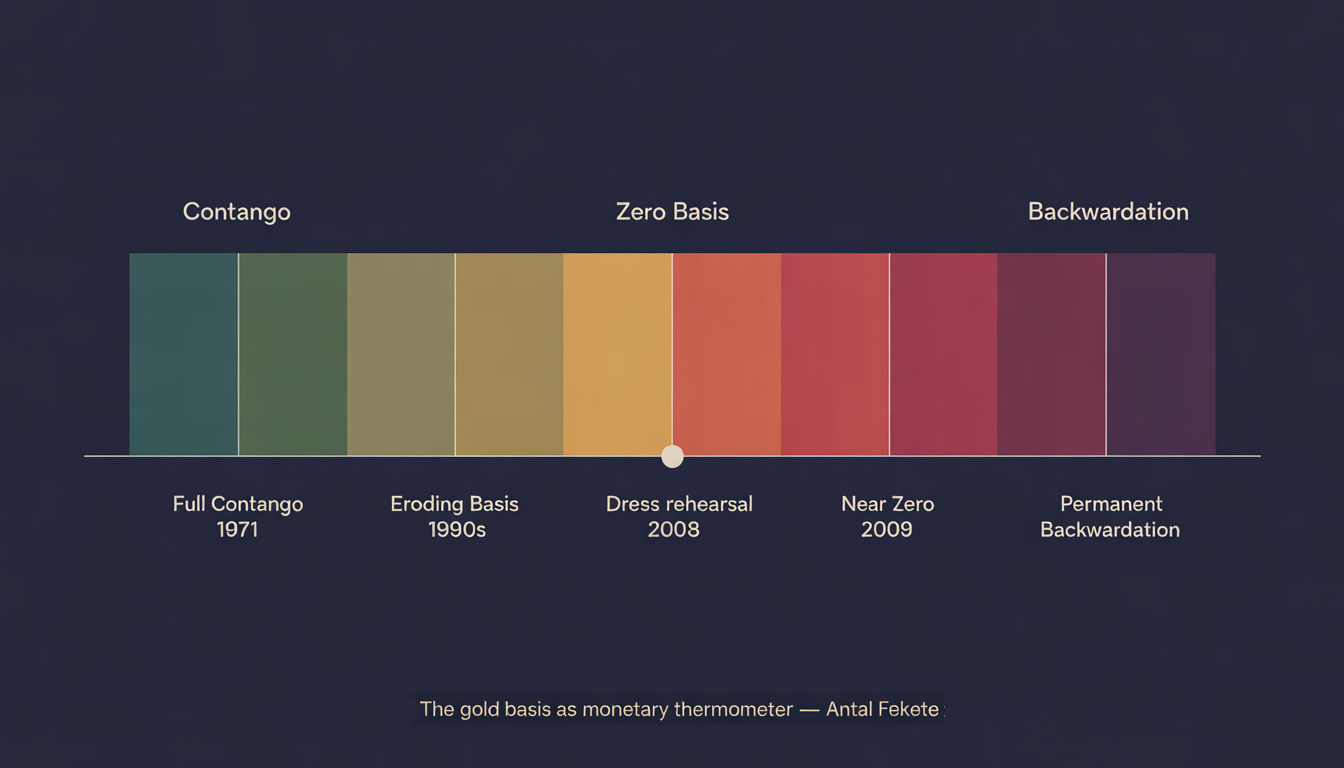

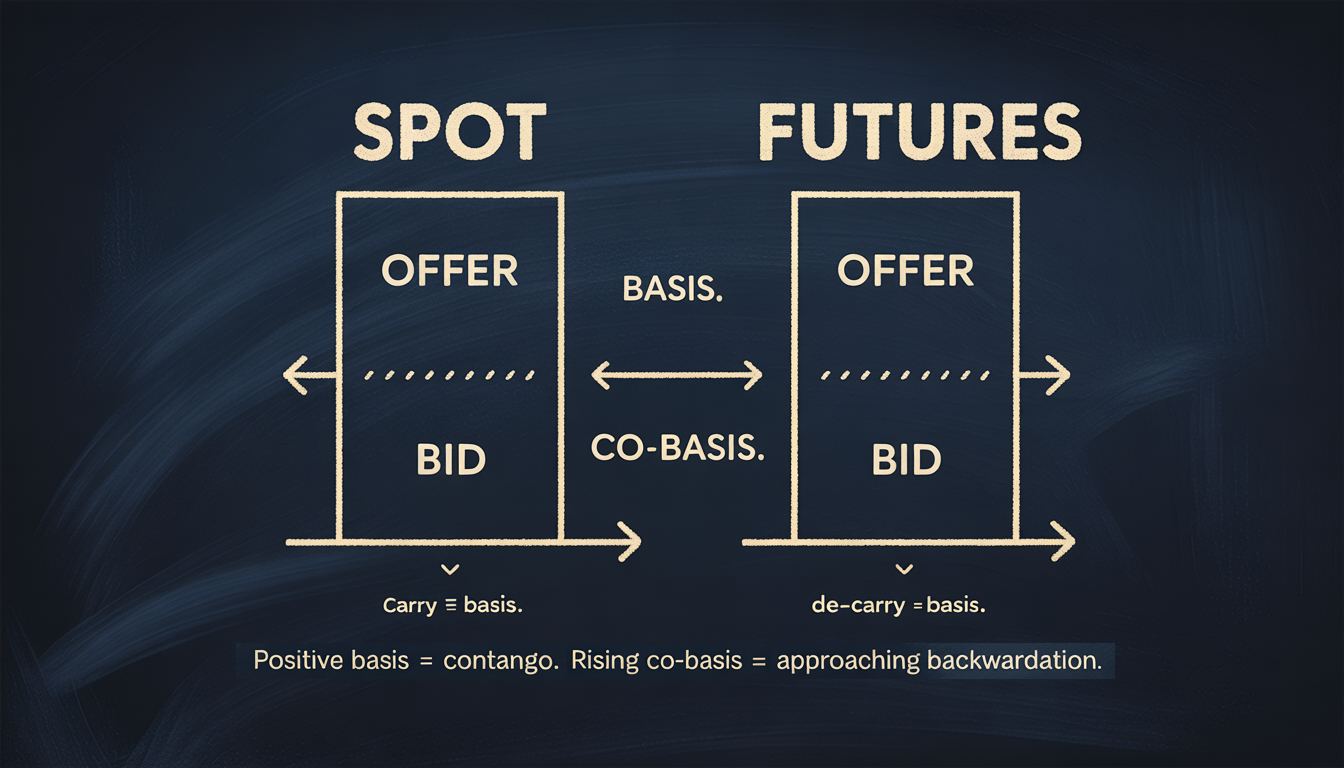

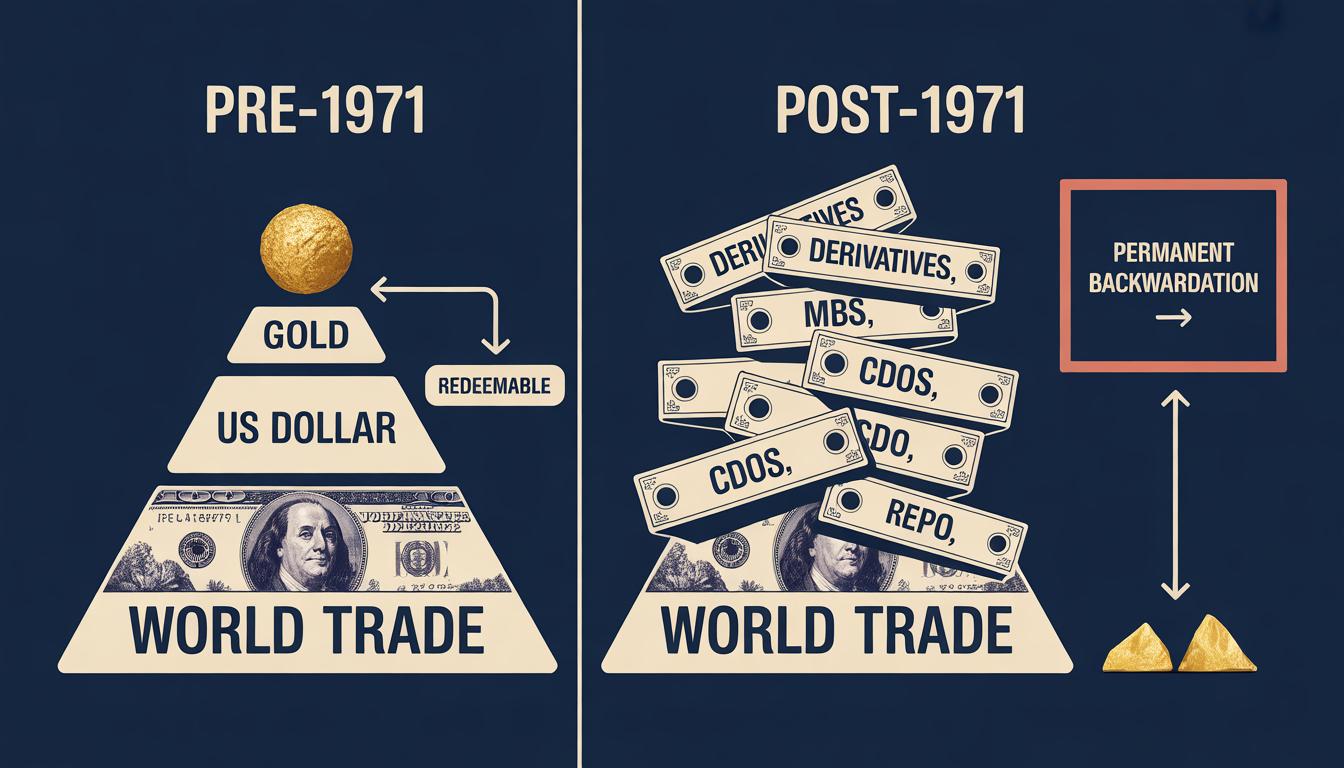

The gold basis is the spread between the futures price of gold and its spot price. In normal conditions — what markets call contango — the futures price exceeds the spot price by approximately the cost of carry: storage, insurance, and the interest foregone by holding metal rather than earning a yield. This premium is the warehouseman's spread, the compensation for providing the service of holding gold today and delivering it later.

When contango narrows — when the futures premium shrinks relative to the full carrying charge — something is signaling. Holders of physical gold are becoming reluctant to lend it into the futures market. The paper promise to deliver gold in the future is commanding less of a premium over gold held in hand. If the basis reaches zero, spot and futures prices are equal: the market places no value on deferring delivery. If the basis inverts — if spot exceeds futures — gold has entered backwardation, a state where physical gold commands a premium over the paper promise. In any other commodity, this is unremarkable; it simply means nearby supply is tight. In gold, whose entire historical role rests on the perfect interchangeability of the physical metal and its paper substitute, backwardation is a different kind of signal entirely.

Fekete had been tracking the basis since 1971. His finding: since that year, when gold futures trading began first in Winnipeg and then in New York, the gold basis had been declining as a percentage of the interest rate. Measured against the full carrying charge, the basis that had once equaled 100% of interest rates had been eroding — decade by decade — toward zero.

"The gold basis is the measure of the extent to which the monetary system is threatened."

Day Two: The Gold Standard and Its Imposters

The second day broadened from the basis to the gold standard itself. Fekete's lecture on The Gold Standard — Truly Out-of-Date or Merely Pushed Aside? distinguished sharply between the genuine article — the Gold Coin Standard, the Unadulterated Gold Standard — and two imposters that masqueraded as equivalents in the twentieth century.

Imposter #1: The Gold Bullion Standard of David Ricardo, implemented in Britain in 1925. This system removed gold coin from everyday circulation, substituting the 400-ounce bar as the smallest gold unit. It aimed at efficiency by eliminating the need for millions of people to hold coins. The effect was to remove the clearing mechanism from the hands of ordinary commerce and concentrate it in institutions. When the system was implemented without the Real Bills infrastructure that gave the genuine gold standard its elasticity, the result — by September 1931 — was the suspension of gold payments and the onset of massive deflation.

Imposter #2: The Gold Exchange Standard, implemented in the United States after 1933. Roosevelt confiscated gold domestically and criminalized private ownership. The dollar remained redeemable in gold internationally — but the gold was double-counted. It served simultaneously as collateral for dollar issuance and as the backing for dollars held by foreign central banks that treated those dollars as "good as gold." Musical chairs: perfectly stable while the music plays, catastrophic when it stops. The music stopped on August 15, 1971.

Rudy Fritsch's contribution on Day Two offered perhaps the simplest formulation of the key distinction: Money is that which extinguishes all debt. Paper, even convertible paper, is a claim on money. Legal tender laws attempt to force the equation of the two. They cannot succeed indefinitely — they merely defer the reckoning.

Sandeep Jaitly extended the technical discussion of the basis into warehousing theory — the formal framework for understanding what the basis and co-basis actually measure and why they move independently. His central point: there are always two prices for gold (bid and offer), and therefore two bases. The carry (basis proper) and the de-carry (co-basis) vary independently and contain different information. The co-basis, which rises as backwardation approaches, is the more sensitive leading indicator.

Day Three: How Falling Interest Rates Destroy Capital

The most analytically dense session of the conference was Fekete's Day Three lecture: How Declining Interest Rates Have Destroyed Capital for the Last Twenty Years.

The argument is counterintuitive at first exposure, but once grasped it reorganizes how you read the entire post-1980 financial history. The mechanism runs as follows.

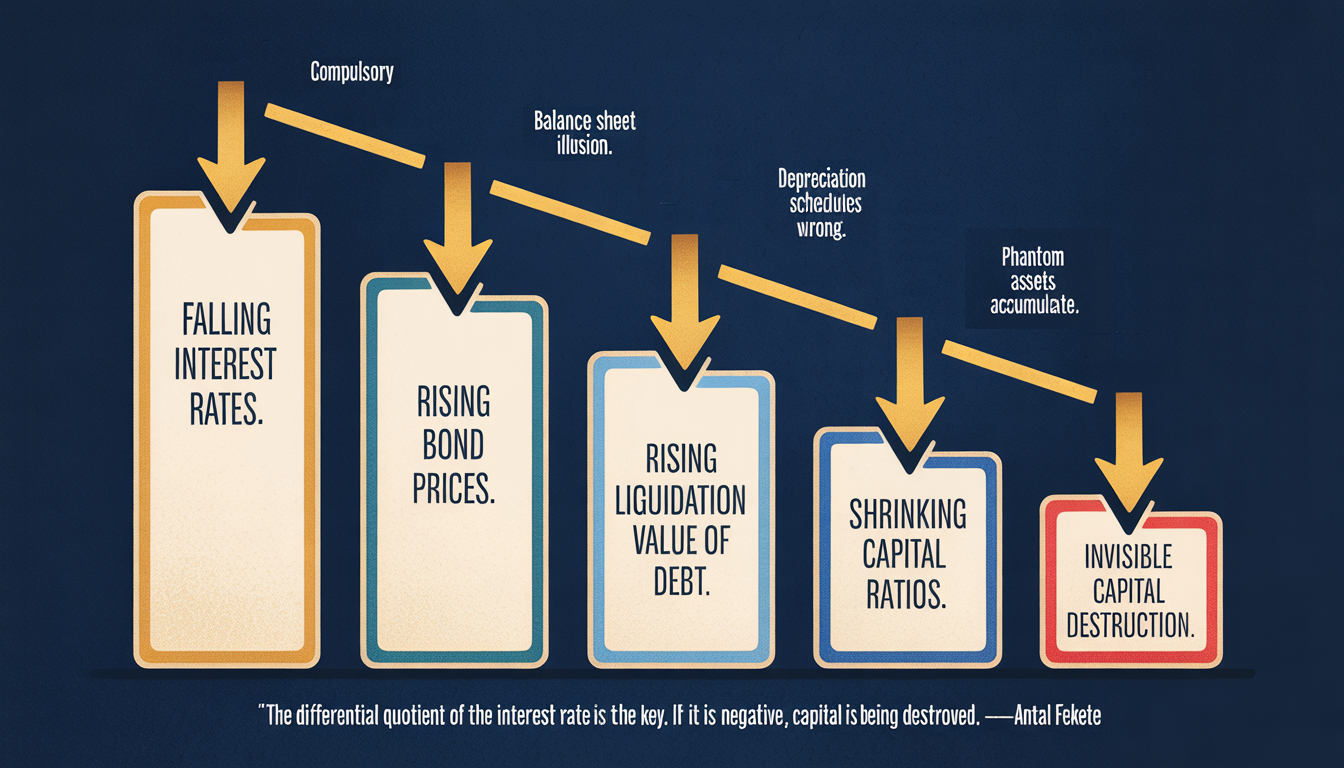

A capital-intensive firm — a manufacturer, an airline, a utility — purchases equipment and depreciates it on a schedule calculated at the prevailing interest rate. The depreciation quota represents the annual charge set aside to eventually replace the asset. Under a stable interest rate regime, the math works: by the time the equipment needs replacing, the accumulated depreciation reserve equals the replacement cost.

But when interest rates fall, the present value of the future stream of payments that the accumulated reserve will generate also falls. The firm now needs a larger reserve to replace the same asset — but the accounting system, based on historical cost, does not automatically adjust the depreciation schedule upward to reflect the new, lower interest rate environment. The firm believes it has capital it does not have. Its balance sheet reports assets that are phantoms.

This illusion is not limited to manufacturers. It afflicts every institution that holds long-duration assets financed at short-duration rates — which is to say, essentially the entire banking system. As Fekete noted:

"The most important holders of bonds are banks. This is the majority of their balance sheet. So as interest rates rose in the early 1980s, bond prices fell and broke the banks. And as interest rates fell for the following twenty-eight years, the illusion of capital abundance masked a slow, continuous destruction of real capital."

The accounting systems in use across the financial world — GAAP, IFRS — do not require firms to adjust their depreciation schedules for changes in interest rates. The result is that the entire post-1980 decline in manufacturing employment, the offshoring wave, the apparent triumph of finance over production — all of these, Fekete argued, were downstream consequences of a capital destruction that no one was measuring because the measurement system itself was built on the assumption of stable rates.

The formula: if the differential quotient of the interest rate is negative (rates are falling), capital is being destroyed. The destruction is invisible until a crisis exposes it. It has been happening continuously since 1981.

Day Four: Permanent Backwardation and What China Should Do

The final day brought the analysis to its terminal point. Nathan Narusis, presenting from a CPA's perspective, provided a sobering quantitative frame: global debt was growing at four to five percent annually while gold production grew at one to two percent. The slow march to a point at which debt cannot be collateralized by gold at any plausible price — permanent backwardation — was not a theoretical endpoint but an arithmetic inevitability, barring a change in monetary regime.

Fekete's own final sessions addressed two questions: what the gold basis tells miners, investors, and traders that the gold price does not; and what China, the world's largest gold producer and one of its largest official-sector gold buyers, should do.

On the first: the gold price, quoted in dollars, is an optical illusion. A rising dollar price of gold may reflect genuine monetary stress or merely dollar weakness. The gold basis strips out the currency noise. A falling basis — gold futures trading at a declining premium to spot — tells you something specific and real: that the willingness of gold holders to extend paper substitutes for their metal is diminishing. This is the signal that matters.

On China, Fekete offered a seven-point program that reads, in retrospect, as a blueprint for exactly what the People's Bank of China has been incrementally doing over the following fifteen years:

- Constitutionally enshrine the right of citizens to save in gold and silver

- Hedge dollar reserve positions with gold purchases announced publicly

- Open the Chinese Mint to free, unlimited, untaxed gold coinage

- Establish the world's first modern gold bank

- Create gold-denominated life insurance, annuities, and pension instruments

- Initiate Real Bills circulation, maturing in gold

- Build the institutional infrastructure for a parallel monetary system

The closing remark was Fekete's, citing Lord Kelvin: "If you can measure something, you can know something. If you cannot measure something, you cannot know anything." The gold basis, he concluded, is the one measurement that the modern monetary system has failed to maintain — deliberately, he suspected, since what it measures is the degree to which that system is threatened.

Looking Back

I left Canberra with a framework that reorganized fifteen years of financial reading. The gold basis, which I had never heard of before arriving, became the lens through which everything else — quantitative easing, the bond market, declining manufacturing, the relentless fall in interest rates — suddenly cohered. Not as separate phenomena requiring separate explanations, but as expressions of a single underlying process: the slow, measured approach of paper gold toward the physical metal, and the monetary reckoning that approach implies.

The participants were few. The ideas were not.

Notes from the 2011 Auckland symposium are collected in Sound Money in Practice: Auckland, 2011.

Related essays

Sound Money in Practice: Auckland, 2011

A week with Antal Fekete and the New Austrian School of Economics in Auckland. The three-legged gold standard, illicit interest arbitrage, gold bonds as a path out of irredeemable debt, and why the unadulterated gold standard is defined not by what it contains but by what it prohibits.

The Golden Triangle: Coin, Bills, Bonds, and the Operational Architecture of a Sound Monetary System

Most modern advocacy for the gold standard describes a monetary regime that is not, and has never been, the gold standard. The picture sketched in libertarian pamphlets and Austrian-tradition advocacy typically consists of paper currency backed by gold reserves held in a vault, with citizens nominally able to redeem notes for gold but rarely doing so. This is not the gold standard. This is the gold-exchange standard, a substitute system constructed at the 1922 Genoa Conference to replace the actual gold standard that the First World War had destroyed in 1914. The actual gold standard — the system that produced approximately a century of price stability, productive investment, and broadly distributed prosperity from the Napoleonic settlement through August 1914 — was a three-pillar operational architecture: gold coin in actual circulation, gold bills clearing short-term commercial transactions, and gold bonds providing the long-term capital and debt-retirement mechanism. Antal Fekete, drawing on Adam Smith's Real Bills Doctrine and Carl Menger's saleability framework, called this architecture the Golden Triangle. His student Rudy Fritsch and others in the New Austrian School have elaborated it. This essay engages the architecture in full: what each pillar was, how the pillars operated together, why the system was destroyed across the 1914-1971 period, and what its restoration would require. The Golden Triangle is not a nostalgic gesture toward a lost monetary regime. It is the operational expression of the saleability framework this catalog has been building from Article 1 forward — and it is the structural alternative to the substitute-layer architecture the catalog's prior thirty-two essays have documented across multiple sectors of contemporary economic life.

Why Gold Didn't Spike: A Fekete Diagnosis of the Iran War

During the 2026 Iran war, gold traded flat and central banks became net sellers. Standard gold-bug frameworks cannot explain this. Antal Fekete's backwardation framework predicted exactly this pattern twenty years ago.