Principles of Economics

Carl Menger · 1871

The founding text of the Austrian School. In 328 pages, Menger overturned the cost-of-production theory of value, established the subjective theory of marginal utility, and showed how money emerges spontaneously from market processes — all without a single equation.

Author

Carl Menger

First published

1871, Vienna

School

Austrian Economics

This edition

Mises Institute, 2007

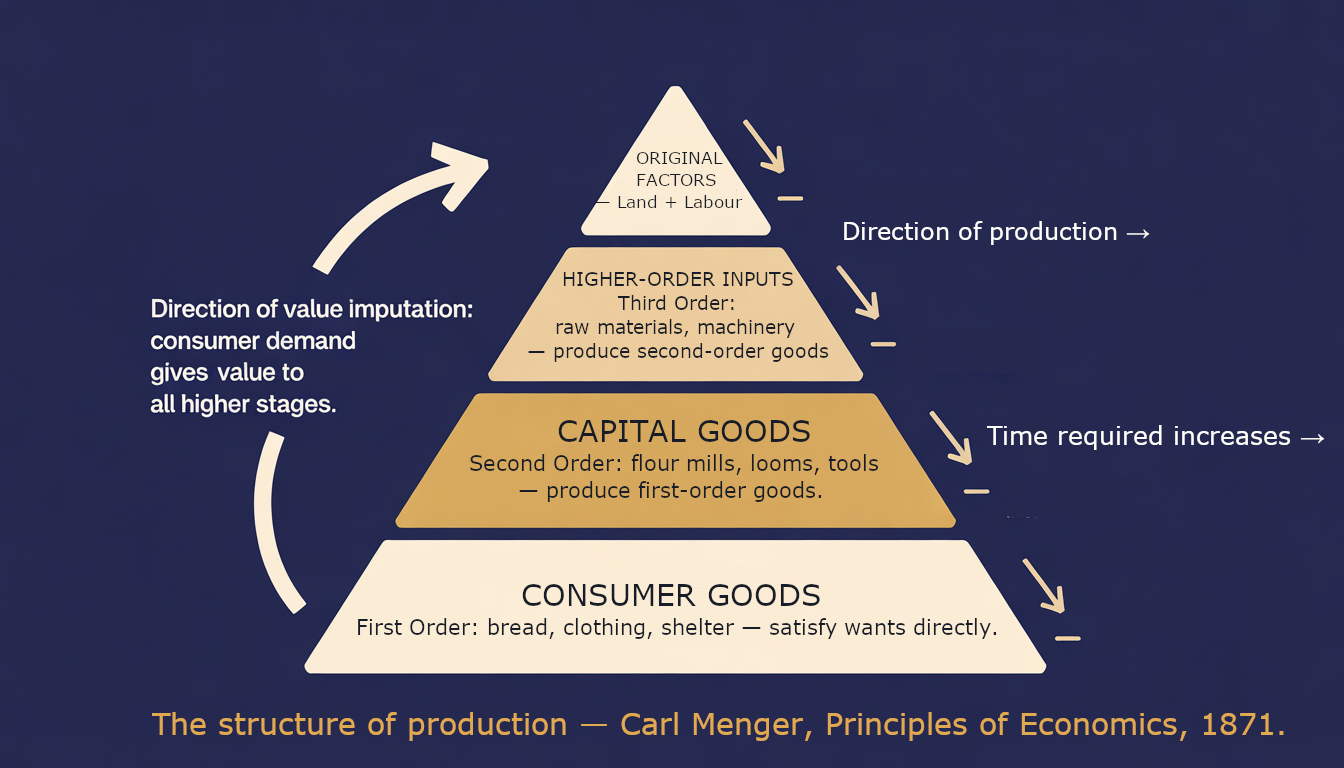

Menger's order of goods: value flows backward from consumer wants through every stage of production — the insight that grounded Austrian capital theory.

Core Concept — The Orders of Goods

Menger's foundational insight: goods exist in a causal order. Consumer goods satisfy needs directly (first order). Capital goods serve to produce consumer goods (higher orders). Value flows backward from consumer needs through the entire chain of production.

Human Need

Hunger, warmth, shelter…

satisfies

First-Order Goods

Bread · Coat · Medicine

Directly consumed to satisfy needs

produced by

Second-Order Goods

Flour · Cloth · Raw Materials

Inputs to produce first-order goods

produced by

Third-Order & Higher

Grain · Farmland · Capital · Labour

Remote causes; value derived from consumer goods

Key implication: The value of a flour mill depends on the value of flour, which depends on the value of bread, which depends on how urgently people want to eat. Capital goods are not independently valuable — their value is imputed backward from final consumption.

Core Concept — Marginal Utility

The value of any unit of a good equals the importance of the least important need it satisfies. As you acquire more units, each additional unit covers progressively less urgent needs.

| Unit | Need it serves (example: water) | Marginal value |

|---|---|---|

| 1st | Drinking — survival | 100 |

| 2nd | Cooking — daily meals | 80 |

| 3rd | Bathing — hygiene | 60 |

| 4th | Watering garden | 40 |

| 5th | Washing carriage← value = this | 20 |

The marginal principle: When you have 5 units of water, the value of each unit equals the 5th unit's value (washing the carriage) — because that is what you would lose if one unit disappeared. This is why abundant water is cheap and scarce diamonds are dear, despite water being more useful overall.

Core Concept — The Spontaneous Emergence of Money

No king, government, or social contract created money. Menger shows how individuals, seeking to trade more effectively, spontaneously converged on the most marketable goods as a medium of exchange.

Barter Economy

Each person must find someone who wants exactly what they have. The "double coincidence of wants" problem severely limits trade.

Highly Marketable Goods Emerge

Some goods (cattle, grain, precious metals) are easier to sell than others. Observant traders start accepting these goods even if they don't need them — because they can trade them later.

Network Effects Amplify the Trend

As more traders accept the highly marketable good, its marketability increases further. Rejecting it becomes costly. The process accelerates through self-reinforcing adoption.

Money

The most marketable commodity becomes universally accepted. No decree required — money is a spontaneous institution that emerges from individual self-interest.

Menger's conclusion: "Money is not an invention of the state. It is not the product of a legislative act, even though the state may endorse and regulate it. It is a social institution that arises from the economic interest of individuals."

Key Ideas

Subjective Value

Value is not inherent in objects but is a relation between goods and human needs. Two people can trade the same object at different valuations — both are correct.

Marginal Utility

A good's value equals the importance of the least urgent need it satisfies. Add one more unit and value falls — it now serves a less pressing need.

Orders of Goods

Capital goods derive their value from the consumer goods they produce. A flour mill's value depends on bread's value, which depends on human hunger.

Spontaneous Money

Money was not invented by authority or social contract. The most marketable goods naturally became money as individuals sought to reduce transaction costs.

Chapter Guide

The General Theory of the Good

pp. 51–76Four prerequisites of goods-character. The hierarchy of orders — bread is first-order, flour second, grain third. Goods derive their value from causal connection to human needs.

Economy and Economic Goods

pp. 77–113Scarcity creates economic goods; abundance creates non-economic goods. Economizing is the rational allocation of scarce means to ends. The origin of economy in scarcity.

The Theory of Value

pp. 114–174Subjective marginal utility. Value is the importance of the least significant satisfaction a good secures. Labour theory of value is refuted — cost follows value, not vice versa.

The Theory of Exchange

pp. 175–190Exchange occurs only when both parties gain. Limits of economically beneficial trade are set by subjective valuations. Mutual benefit, not exploitation, defines the market.

The Theory of Price

pp. 191–225Prices emerge from individual valuations under isolated exchange, monopoly, and bilateral competition. Prices are not set — they are discovered through the exchange process.

Use Value and Exchange Value

pp. 226–235Two forms of the same phenomenon. Use value: goods satisfy needs directly. Exchange value: goods obtain other goods through trade. Both are expressions of subjective importance.

The Theory of the Commodity

pp. 236–256Marketability (Absatzfähigkeit) — how easily a good can be sold at its full value. Goods vary enormously in saleability. This difference explains why some become money.

The Theory of Money

pp. 257–285The most marketable commodities become money through individual self-interest. No authority or social contract needed — money is a spontaneous market institution.

Why It Matters

Before Menger, economists explained value through the amount of labour embedded in a product. Ricardo and Marx built vast systems on this foundation. Menger demolished it in his first chapter: value originates in the subjective importance of human needs, not in objective production costs.

Simultaneously — and independently — William Stanley Jevons in England and Léon Walras in Switzerland reached similar conclusions about marginal utility. The "Marginal Revolution" of 1871 transformed economics. But where Jevons and Walras expressed their theories mathematically, Menger remained resolutely verbal and causal — a choice that shaped the entire Austrian tradition.

The implications remain radical today: prices are not set by costs, wages are not set by labour, and money was not created by government. All are spontaneous market outcomes. Menger's framework gave subsequent Austrians — Böhm-Bawerk, Mises, Hayek — the foundation for capital theory, business cycle theory, and the critique of central planning.