Whither Gold?

Antal E. Fekete · 1996 · Winner, International Currency Prize

Winner of the 1996 International Currency Prize, sponsored by Bank Lips, Zürich. Written at Memorial University of Newfoundland.

The Argument

The gold standard is not about price stability.

For decades, economists have attacked and defended the gold standard on the wrong grounds — price stability. Fekete argues the standard's essential function is entirely different: it holds the interest-rate structure at the lowest level compatible with economic conditions, keeping debt within limits. Without it, rising and gyrating interest rates destroy capital values, and the world's debt tower grows until it must collapse.

"This essay intends to show that the essence of the gold standard is not to be found in its ability to stabilize prices — that is neither desirable nor possible. It is to be found in its ability to stabilize the interest-rate structure at the lowest level compatible with economic conditions, and thereby to keep debt within limits."

Key Ideas

The True Function of Gold

The gold standard does not — and cannot — stabilize prices. Its essential function is to stabilize the interest-rate structure at the lowest level compatible with economic conditions. This is what makes capital formation possible.

Constant Marginal Utility

Gold is unique among commodities: no one ever has enough of it. This constant marginal utility means the Mint can be opened to unlimited free coinage without price distortions — the property that makes gold suitable as money.

The Unpayable Debt Tower

Under irredeemable currency, a debt of $x can never be liquidated — only transferred to another debtor. The world's total indebtedness can grow without limit. The only exits are default or currency depreciation.

Gold-Bonded Debt

The mechanism that made the gold standard self-regulating was government debt denominated in gold. It tied the cost of borrowing to real productive conditions and capped the total debt governments could accumulate.

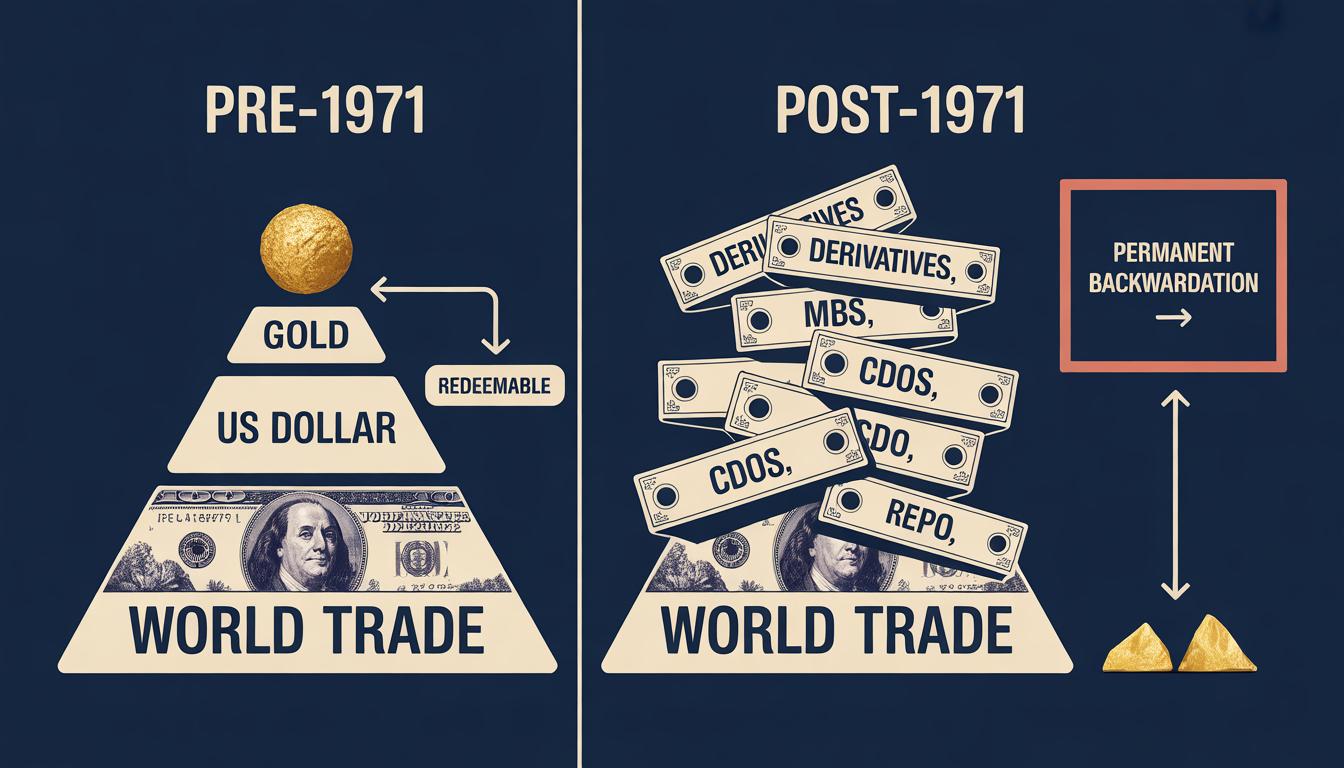

Before 1971: gold anchored the dollar anchored world trade. After 1971: a tower of derivative claims piled on severed foundations — and permanent backwardation as the terminal horizon.

The Mechanism

Gold Standard

Free coinage + gold bonds

Interest rates stable at minimum

Irredeemable Currency

No gold anchor

Interest rates gyrate + rise

Under gold:

Debt remains bounded

Governments can borrow, but gold bonds discipline the cost

Without gold:

The Tower of Babel

Total indebtedness can only rise — default or depreciation are the only exits

Section Guide

Introduction

The 1971 severance of money from gold had two immediate, ignored consequences: the world lost the ability to reduce total indebtedness through normal payments, and countries lost the option to balance current accounts. Every dollar paid to retire a debt is merely transferred to another debtor — never extinguished.

1 — A Brief History of Money

From Menger's marginal utility to the demise of bimetallism: Fekete traces how gold's constant marginal utility made it uniquely suited to be money, how plunder (ancient and modern) corrupted monetary standards, and how the market — not governments — demonetized silver in the 1870s.

2 — Towards a New Theory of Interest

The heart of the essay. Fekete introduces the concept of "squaring the diagonal" — the exchange of present income for future wealth — and shows that the interest rate under a gold standard is held at its natural minimum. Without gold, rates gyrate and destroy capital.

4 — Whither Gold?

The policy prescription. Fekete argues for reopening the Mint to gold coinage, reintroducing gold-bonded government debt, and restoring the real bills market. Until then, the debt tower's collapse is only a matter of time.