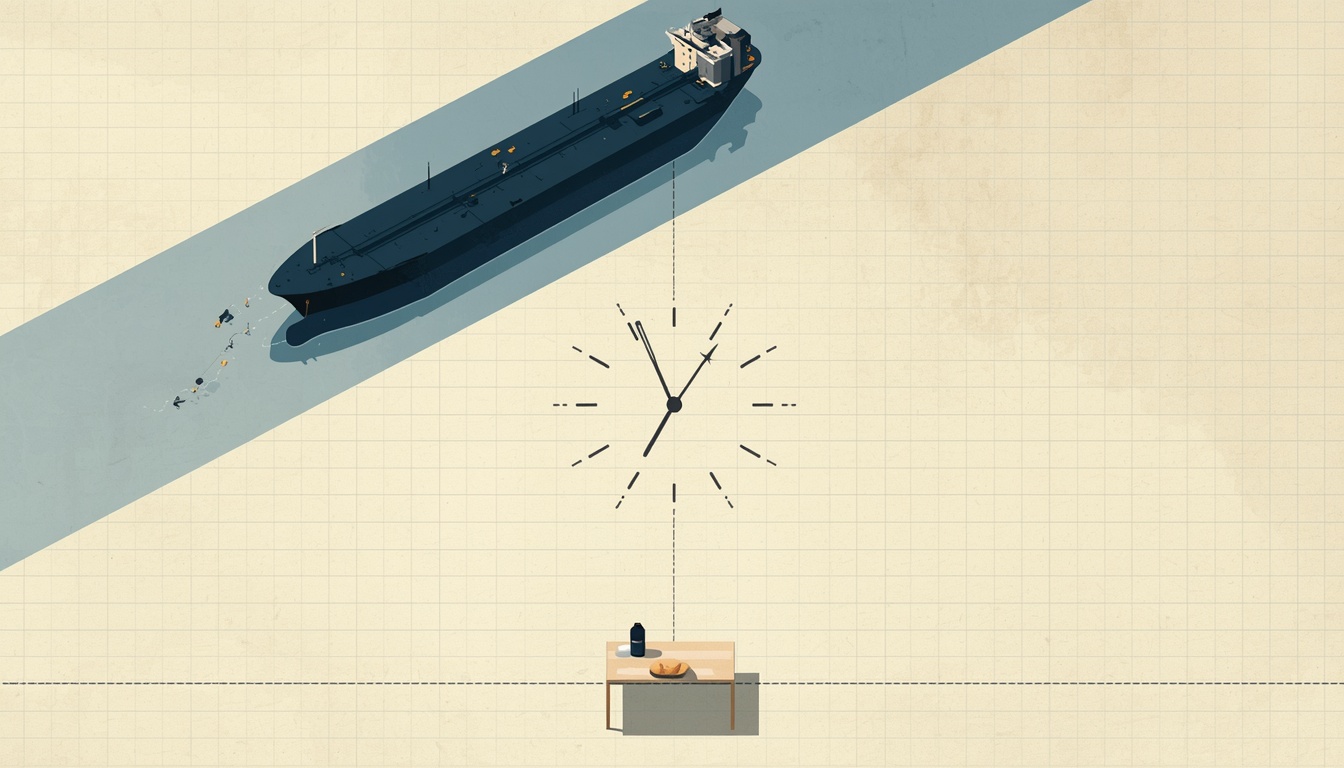

The Lag

Supply shocks propagate to consumer prices on calendar time, not news-cycle time. The Strait of Hormuz closure that began on February 28 is now four months into a propagation sequence whose academic-literature pass-through estimates point to peak American household impact in Q1–Q2 2027 — twelve to fifteen months after the shock began, and substantially after any plausible geopolitical resolution. The strategic reserves are not absorbing the disruption; they are deferring it. The framework reads the lag as the structural mechanism.

Full analysis: newaustrianeconomics.com/forum/26-hormuz-lag-household-cost

Welcome to Issue #006 of The Dispatch. Each Monday, this letter takes one situation from the week's news and reads it through the lens of Carl Menger and Antal Fekete — paired with a foundational concept, a snapshot of this week's dashboard readings, and a piece from the archive. If someone forwarded this to you, subscribe here.

The Lens

On February 28, 2026, U.S. and Israeli forces launched coordinated strikes against Iranian nuclear, military, and IRGC command infrastructure. Within forty-eight hours, the Strait of Hormuz — the maritime chokepoint through which approximately 20 million barrels per day of oil and approximately 20% of global LNG transit — had effectively closed to commercial shipping. Major carriers (Maersk, MSC, CMA CGM, Hapag-Lloyd) suspended transits within the same window. War risk insurance was cancelled for Gulf transits on March 5. The United States released 172 million barrels from the Strategic Petroleum Reserve in March 2026 as part of a coordinated 400-million-barrel IEA response — the largest such coordinated release in history. The SPR now sits at approximately 243 million barrels, its lowest level since February 1982. Brent crude is up approximately 60% since the strikes began.

Yet U.S. consumer price inflation prints have remained moderate through April (3.8% headline, 2.8% core). The popular financial press has treated the absence of an immediate price spike as evidence the disruption is being managed.

This reading misunderstands the calendar mechanics. Supply shocks propagate to consumer prices on calendar time, not news-cycle time — and the propagation schedule is not negotiable.

Lead Essay: The Lag Is the Structure

The framework's analytical posture across this catalog has consistently been that the aggregates the financial press and policy community track are structurally inadequate to capture the timing and distribution of economic stress as it actually arrives at the household level. The QE-to-inflation lag of 2008–2022 was the canonical demonstration for a monetary shock: the Federal Reserve expanded its balance sheet from approximately $900 billion to $4.5 trillion through 2008–2014, and the peak headline CPI of 9.1% arrived in June 2022 — approximately fourteen years after the expansion began and eight years after the expansionary phase ended. The post-COVID monetary expansion compressed this somewhat, with consumer price effects arriving within eighteen to twenty-four months. The Hormuz disruption of 2026 is a structurally different shock — supply-side rather than monetary — but the calendar mechanics of propagation are similar in form.

Two mechanisms produce the systematic lag. The buffer mechanism (strategic reserves, commercial inventories, hedging programs, contract carry-over) absorbs the initial shock and allows the underlying disruption to operate for weeks or months before propagation reaches retail prices. The contract mechanism (multi-month and multi-year forward contracts at fixed prices, hedging programs structured 6–24 months forward) defers the effect of current spot-market changes onto future periods when contracts come up for renewal. The combined effect is what economists call pass-through lags. The academic literature is substantial on this point.

The empirical pass-through estimates are specific. Galo Nuño's 2009 Energy Economics study found that direct oil-to-refined-product pass-through completes within three to five weeks. The more consequential pass-through, from refined products and primary inputs to broader consumer goods, operates on substantially longer timelines. Robert Minton (Federal Reserve) and Brian Wheaton (UCLA) in 2024, using detailed input-output data, found that upstream industries feel approximately 75% of an oil price shock within six months, while downstream industries take approximately twenty months to feel a similar magnitude of impact. The Federal Reserve's own modeling estimates that a permanent 10% increase in crude oil prices adds approximately 0.4 percentage points to headline CPI over the course of one year — each year — meaning the full cumulative pass-through extends across multiple years rather than completing within twelve months.

Combining these empirical estimates with the current shock: Brent crude is up approximately 60% from pre-conflict levels. If the disruption persists, the cumulative consumer price impact would be approximately 2.4 percentage points added to headline CPI over the propagation window. The window itself peaks in Q1–Q2 2027.

The channel-by-channel propagation timeline runs from days (gasoline pump prices, T+0 to T+6 months, peak ~May–June 2026) through years (manufactured goods, T+5 to T+22 months, peak ~T+12; pharmaceuticals, T+6 to T+24 months). The most economically consequential single channel and the one the framework reads as most underappreciated is fertilizer-to-food. Approximately one-third of globally traded fertilizer transits the Strait of Hormuz. Natural gas is the primary feedstock for nitrogen fertilizer production — and natural gas prices are themselves rising through the LNG channel. Fertilizer accounts for roughly one-third of the cost of corn and wheat production. The lag is dominated by the agricultural growing cycle: fertilizer purchased for 2026 was largely contracted before the disruption began, with effects flowing into 2027 plantings, into 2027 harvests, and into 2027–2028 food prices. The framework's reading: U.S. grain prices will rise approximately 25–40% by mid-2027 due to the fertilizer transmission alone, with broader food price impacts following.

The buffer math is sobering. Combined IEA member emergency stocks plus industry stocks of approximately 1.8 billion barrels are being drawn down at a rate that gives perhaps 6–12 months of effective absorptive capacity. The SPR specifically is at 35% of capacity, structurally compromised by repeated drawdown cycles, with refilling on a 2026–2029 timeline. Cushing, Oklahoma — the central U.S. oil storage hub — is approaching operationally low levels. The buffers are deferring impact during 2026; the impact arrives in 2027 as the buffers exhaust.

The geopolitical structural reading argues against clean resolution. China loses from the disruption but gains nothing from supporting its resolution; Russia benefits directly from elevated oil prices; Iran's IRGC has incentive to maintain disruption capability as leverage; war risk insurance markets re-establish coverage slowly even after formal de-escalation. The combined effect: the disruption will likely persist at meaningful intensity through the second half of 2026, with partial improvement through 2027 and full normalization not before 2028 at the earliest — substantially independent of any specific resolution scenario that may emerge.

The framework's specific forecast, recorded for testing: pump prices elevated $1.20–$1.80 per gallon by mid-2026; headline CPI rising to 4.5–5.5% by Q3 2026 and 5–6% by Q4; food inflation accelerating from 2.6% to 4–5% through 2026 and reaching 6–9% year-over-year by mid-2027; manufactured goods showing 5–10% real price increases through 2027; headline CPI peaking in the 6–7% range in Q1–Q2 2027 and moderating to 4–5% through 2028. By the time the May 2027 CPI release confirms what the framework predicts now, the American household will have been absorbing the impact through grocery store visits, pump fillings, utility bills, durables purchases, and service prices for nine to fifteen months.

→ Read the full analysis: The Lag: What Hormuz Will Cost the American Household, and When — The Forum

Concept in Focus: The Mengerian Stress Index

The third essay of this catalog proposed a quantifiable extension of Menger's saleability spectrum — five observable market proxies, each capturing a different dimension of substrate-layer trust, aggregated into a composite stress reading that would lead conventional crisis indicators by several weeks. The proposal was theoretical.

As of this week, it is no longer. The composite Mengerian Stress Index (MSI) runs live on the toolkit, updated continuously across four operational components (a fifth is in build): the gold basis, the silver/gold ratio, ETF NAV deviation across precious-metals trackers, and the FX cross-currency basis (CIP-deviation) on the dollar against major currency pairs. Each component is a direct-observation measure of substrate fragility in a specific market. The composite Z-scores them against rolling history and aggregates them into a single regime classification.

The accompanying Forum essay has been reworked from spec into the public definition layer for the live framework. It now contains precise definitions for each of the five proxies, the motivation for the composite, the marketability half-life as a regime-classification tool, and explicit acknowledgment of which calibration details sit behind the dashboard rather than in the public-facing essay. The live MSI lives at /toolkit/mengerian-stress-index/. The definitional essay lives at Forum #12.

The framework's broader analytical claim is that aggregates lie because they smooth across heterogeneity that matters. The MSI is the framework's affirmative answer — a composite that integrates the heterogeneity the conventional aggregates obscure, reported with the regime classification that household and operator decisions actually need.

The Atlas page on the Austrian Business Cycle covers the underlying theory of how substrate-layer stress accumulates into the cyclical patterns the MSI is calibrated to read.

The Dashboard

A new recurring section: each week's MSI composite and three readings tied to the issue's theme. Snapshot from the live toolkit as of June 1, 2026.

- Mengerian Stress Index (composite) — 2.38 / elevated (3 of 4 components operational; ETF NAV Deviation in build). The framework's headline composite reading just went live this week. The current value is well outside the normal range, driven primarily by the FX cross-currency basis component and elevated repo-haircut dispersion. → /toolkit/mengerian-stress-index

- Gold Basis — −0.685% (backwardation) — spot $4,545.95 (LBMA PM 2026-05-29), /GC front-month $4,514.80, basis −$31.15. Substrate-trust signal between LBMA spot and COMEX front-month, the same diagnostic Issue #001 introduced. Futures below spot is Fekete's "pristine, incorruptible measure" of paper-money stress. The reading is modest in magnitude but in the wrong direction. → /toolkit/gold-basis

- Silver/Gold Ratio — 60.08 — gold $4,514.80, silver $75.15. Bimetallic stress reading. Silver remains relatively elevated against gold even four months after the January 30 paper-physical decoupling event (Issue #005), with the ratio still below the long-run norm of ~70. Recovery is partial, not complete. → /toolkit/silver-gold-ratio

- FX Cross-Currency Basis — 855 bps mean absolute deviation across four pairs (EURUSD +688, GBPUSD −111, USDCHF +1,951, USDJPY +673), Z-scored at the framework's +5 cap. Dollar-liquidity stress. Normal CIP deviation runs single-to-low-double digit bps; the current reading is two orders of magnitude outside that range. The Hormuz disruption is drawing on global dollar reserves through the energy-import channel, and this is where the pressure registers first. → /toolkit/cross-currency-basis

The dashboard runs continuously; the snapshot here is the framework's reading at publication. Subscribers tracking the trajectory should bookmark the toolkit and check between issues.

The Actionable

The framework's specific operational observations for households exposed to the Hormuz propagation:

- The aggregate price data will report this on lag. Headline CPI will not reflect full impact until 9–15 months after the household begins experiencing it through retail purchases. Households waiting for aggregate confirmation before adjusting planning will be making decisions on data that materially understates current cost pressure. Use forward-looking channel-specific signals (gasoline futures, LNG benchmark prices, container shipping indexes) as leading indicators rather than relying on aggregate inflation reports.

- The inventory cycle is currently working in your favor for one-time purchases. Vehicles, appliances, electronics, and similar durables in 2026 retail were produced under pre-shock cost structures. Replacement inventory produced in 2026 under elevated input costs reaches retail through 2027. Households contemplating large durable purchases should price the buffer-exhaustion timeline explicitly.

- Fertilizer and food are the highest-leverage channels. The fertilizer-to-food propagation through the 2027 planting cycle is the most economically consequential single channel and the hardest to escape through individual household preparation. Households with significant exposure (large families, fixed incomes) should anticipate meaningfully tighter budgets through 2027 and consider whether existing food-spending categories can be reconfigured before the impact arrives.

- The strategic petroleum reserve is at near-operational lows. Households whose planning assumed continued availability of reserve releases as a price-stabilization mechanism should recalibrate. Any subsequent disruption arriving before the reserve is rebuilt will face substantially less buffer than what muted the early-stage Hormuz impact.

- The MSI is the standing diagnostic. The Dashboard above is where the framework reads substrate-layer stress in real time. As Hormuz propagation compounds with the housing diagnostics (Issues #003–#004), the precious-metals substrate (Issue #005), and the cryptocurrency-architecture pressure (Issue #002), the composite reading is the integrated signal.

Educational content only — not investment advice.

From the Archive

"The QTM is a linear model that may be valid as a first approximation, but fails in most cases as the real world is highly non-linear. My own theory predicts that it is not hyperinflation but a vicious deflation which is in store for the dollar... While prices of primary products such as crude oil and foodstuffs may initially rise, there is no purchasing power in the hands of the consumers, nor can they borrow as they used to do in order to pay the higher prices."

— Antal Fekete, A Critique of the Quantity Theory of Money (April 2009)

Fekete's 2009 critique was that the Quantity Theory of Money — the framework underlying both monetarism and modern central banking — treats monetary propagation as if it were a linear function of money supply, when the real world is governed by structural mechanics (bond speculation, falling-rate distortions, capital erosion) that the theory smooths over. The same critique applies, with the variables changed, to the conventional reading of supply shocks. The conventional reading treats Hormuz propagation as if it were a short-window function of the shock; the framework's reading is that the structural mechanics (buffer exhaustion, contract carry-over, channel-by-channel pass-through asymmetries) govern the actual trajectory in ways the simple model cannot capture. The lag is the structure, not a delay in an otherwise linear process.

→ Read the full essay in the Fekete Archive

Also This Week

A heavy week of catalog and toolkit work:

- Companion piece: The Iran Crypto Seizures and the Privacy Narrative — Treasury Secretary Scott Bessent at the Reagan National Economic Forum on May 29: "We just outright grabbed the wallets. Some of them may be typing in right now and might not realize their wallet had been grabbed." The framework's reading of the cleanest single empirical demonstration that cryptocurrency's privacy and censorship-resistance properties are sharply heterogeneous across instrument types — and that the Cryptocurrency Trilogy's (Issues #002, Forum #13–#15) abstract arguments are now operationally validated.

- From spec to live: The Mengerian Stress Index — Forum #12 has been reworked from theoretical specification into the public definition layer for the now-live framework. Precise component definitions; the composite motivation; the marketability half-life as regime classification. Calibration details remain behind the dashboard, where they belong.

- Toolkit infrastructure: A substantial portion of the toolkit went live this week. Phase 1 instruments (Gold Basis, Silver/Gold Ratio, Yield Curve, Time Preference, Business Cycle, LBMA Fixes) are now live with real continuous data. Phase 2 instruments wired to the API (FDIC Failures, COMEX Paper/Physical, COT Concentration, Repo Haircut, Treasury Auction Stress, Property Tax Projector, more). Wave 1 additions: Enforcement Watchlist, Metro Saleability Map. The composite MSI itself is now operational. The full instrument list is at /toolkit. Phase 3 instruments are in build.

- Atlas: The Austrian Business Cycle — the underlying theory of how substrate-layer stress accumulates into the cyclical patterns the MSI is calibrated to read.