On the Origins of Money

Carl Menger · 1892 · Economic Journal, Vol. 2

The Argument

Money was not invented. It was discovered.

No government created money. No social contract invented it. No individual planned it. Money emerged spontaneously from barter through the rational self-interest of individual traders, each seeking to widen their exchange possibilities by accepting the most saleable commodity available. Menger's 1892 essay is the proof — and it dismantles every theory of money that begins with the state.

"Money has not been generated by law. In its origin it is a social, and not a state institution. Sanction by the authority of the state is a notion entirely foreign to it."

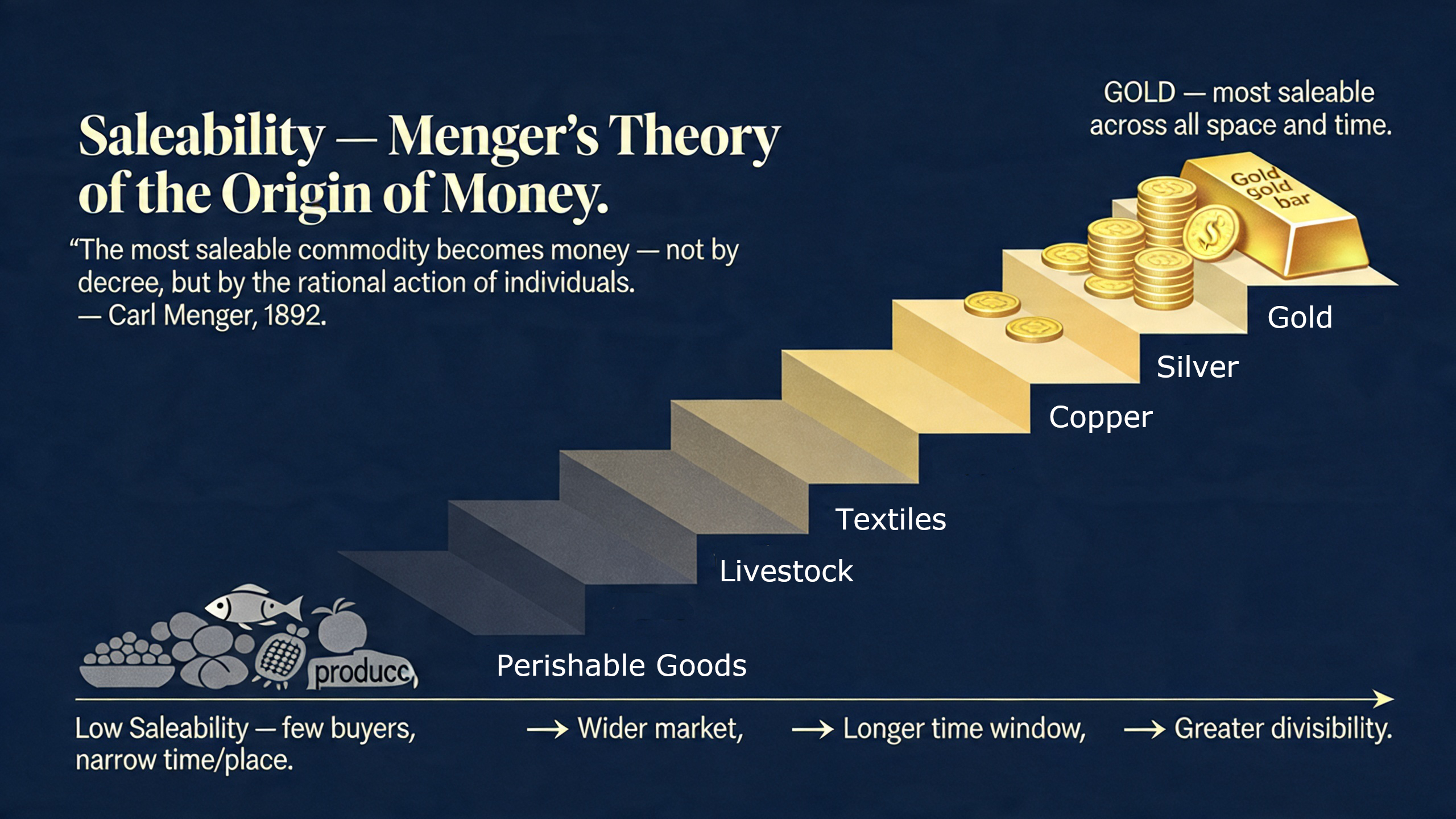

Menger's saleability spectrum: the good most easily exchanged across the widest range of people, places, and times becomes money.

Listen

Audio reading

On the Origins of Money

Read by Jason

Full reading of all nine chapters plus foreword — approx. 2 hrs.

How Money Emerges — Menger's Model

Barter

Double coincidence of wants limits exchange

Most Saleable Commodity

Traders accept it to re-exchange, not use

Imitation Spreads

Others copy the profitable practice

Money Emerges

Gold accepted universally — no decree needed

No central authority required at any stage. The process is entirely market-driven.

Chapter Guide

Foreword by Douglas E. French

pp. 7–9French contextualizes Menger's essay for the modern reader: governments have so thoroughly controlled the money narrative that the public no longer understands what money actually is or where it came from. Menger's answer — spontaneous market emergence — remains the only honest account.

Introduction

pp. 11–13Menger opens with a puzzle economists had long dodged: why do all economizing individuals willingly accept certain commodities in exchange for their own goods, even when they have no direct use for those commodities? This is the origin-of-money problem, and no satisfactory answer existed in 1892.

Attempts at Solution Hitherto

pp. 15–17Previous theories held that money arose from a social contract or government decree — that men simply agreed to use gold as money. Menger demolishes this: agreement theories explain nothing, because they presuppose the very problem they claim to solve. Why would a pre-monetary society agree to use *this* commodity rather than any other?

The Problem of the Genesis of a Medium of Exchange

pp. 19–21Menger sharpens the problem. In a barter economy, exchange is cumbersome: a man who has shoes but wants bread must find someone who has bread *and wants shoes*. The double coincidence of wants severely limits trade. How did the transition to indirect exchange — through a common medium — come about, without central direction?

Commodities as More or Less Saleable

pp. 23–27The key insight: commodities differ in their *saleableness* — how easily they can be sold at the prevailing price at any time and place. Some goods find buyers quickly in large quantities with little price concession; others do not. Saleableness is the crucial asymmetry that drives monetary emergence.

Concerning the Causes of the Different Degrees of Saleableness

pp. 29–31What makes a commodity highly saleable? Menger identifies several causes: being demanded by many people, being durable, divisible without quality loss, easily transported, having a stable price, and having demand spread across space and time. Precious metals score well on every dimension — especially gold.

On the Genesis of Media of Exchange

pp. 33–37Here is Menger's solution. No decree was needed. The most economically aware traders, seeking to widen their trading possibilities, began accepting highly saleable commodities — not for their own use, but to re-exchange them. Their success was visible to others, who imitated the practice. Money emerged through *imitation of the profitable*, not agreement or command.

The Process of Differentiation

pp. 39–43Once a commodity gains wide acceptance as a medium of exchange, network effects reinforce its position: the more people who accept it, the more valuable it is to accept it. This process of differentiation explains why monetary systems converge on a single medium rather than persisting with many competing ones.

How the Precious Metals Became Money

pp. 45–49Menger applies his framework to the historical facts. Gold and silver, independently of government action, became money in every advanced civilization because their natural properties — durability, divisibility, portability, homogeneity, and scarcity — maximized saleableness. The discovery was made in every corner of the ancient world.

Influence of the Sovereign Power

pp. 51–55Government did not create money; it arrived late and found money already operating. What sovereigns did was stamp coins to certify weight and fineness — useful, but secondary. When governments abused this power to adulterate the currency, they did not create a new money; they debased the one the market had already chosen.

Why This Essay Matters

Every debate about monetary policy — central banking, inflation, cryptocurrency, gold — ultimately comes back to a prior question: what is money, and where did it come from? Menger's answer determines everything that follows. If money is a market institution, then central banks are an intrusion into a spontaneous order. If it is a state institution, then government has legitimate authority over the monetary system.

Fekete's entire body of work — the real bills doctrine, the gold basis, the theory of interest — rests on Menger's foundation. So does Mises's regression theorem. Reading this essay is not optional background reading. It is the starting point.

Continue Reading