The April 2026 nonfarm payrolls report, released by the Bureau of Labor Statistics on May 2, looked relatively healthy: 115,000 jobs added, unemployment unchanged at 4.3%, with the year-to-date monthly job growth average reaching 76,000 — substantially better than the anemic 10,000 monthly average that characterized 2025. The conventional reading, repeated across financial press in the days following, was that the labor market was "healing" after the post-pandemic adjustment cycle and that the broader economy was demonstrating resilience despite the Iran conflict's energy price pressures.

The framework's reading is different, and structurally so. The 115,000 jobs added in April were not distributed across sectors in the way the prior labor market expansion was distributed. Healthcare added 37,000 jobs. Transportation and warehousing added 30,000. Social assistance trended up. These three categories alone accounted for nearly 60% of the headline number. The contributions from technology, professional services, financial services, marketing, and other knowledge-work categories that historically drove labor market expansions were either flat or modestly negative. The aggregate looked healthy because the growth in physical-presence and care-economy work substantially offset the contraction in AI-substitutable knowledge work. The aggregate is concealing a structural transformation, not reflecting a recovery.

Through the first quarter of 2026, the U.S. technology sector saw approximately 45,000 layoffs, with approximately 9,200 — roughly 20% — explicitly attributed by the employer to AI and automation decisions. The share attributable to AI was rising quarter over quarter. The 2025 full-year U.S. layoff total was approximately 1.1 million; tech-sector layoffs for 2025 were 170,630, with approximately 55,000 directly attributable to AI substitution decisions by the companies announcing them. Meanwhile, the construction sector was short approximately 349,000 workers in 2026 alone, with the shortfall projected to climb to 456,000 by 2027 and to 2.1 million skilled trades positions unfilled by 2030. Ford CEO Jim Farley reported on a January 2026 podcast that his company had 5,000 open mechanic positions it could not fill — at salaries reaching $120,000 per year, nearly double the $62,000 national median. Data-center electricians were earning $280,000-plus. BlackRock CEO Larry Fink committed $100 million to training programs, citing his concern that "we're going to run out of electricians" needed to build AI data centers. Total corporate pledges for skilled trades training reached $365 million by mid-2026.

These two patterns are operating simultaneously in the same labor market. They are not in tension; they are the same phenomenon viewed from opposite sides. The framework's central observation: the Mengerian saleability spectrum of human labor is being structurally reordered in real time, with the work that AI can substitute losing saleability and the work AI cannot perform gaining it. The aggregate "labor market" is the wrong unit of analysis for what is happening. The structural reading requires decomposition by saleability profile, not aggregation by headline employment count.

This essay is the twelfth installment of Watching the Cracks. It does four things. First, it engages the most consequential single statement made about labor markets by an AI industry leader in this cycle — Dario Amodei's "white-collar bloodbath" prediction — directly and honestly. Second, it applies Menger's six saleability criteria to labor itself, treating human-hours-of-work as an asset class whose monetary properties can be evaluated through the same framework the catalog has applied to housing, precious metals, cryptocurrency, and other instruments. Third, it documents the specific empirical decomposition of the 2026 labor market, identifying which categories are gaining and losing saleability and at what rates. Fourth, it traces the broader monetary-architectural implications through Cantillon's distributional analysis and connects to the catalog's prior work on credential erosion (Article 23) and the broader substrate-fragility thesis.

A note on framing before proceeding. The framework's intellectual posture throughout this catalog has been to engage substantive claims honestly even when they run against the interests of specific institutions, including Anthropic itself. The Cryptographic Marketability Premium essay (Article 6) did this with respect to AI capability concentration. The Iran crypto seizures essay (Article 25) did this with respect to the limits of cryptocurrency's privacy properties. This essay does it with respect to AI's labor-substitution effects, which Anthropic both publicly acknowledges (Amodei's statements) and structurally benefits from (more capable AI substitutes more labor; more labor substitution accelerates AI adoption). The framework's reading is the framework's reading.

Engaging Amodei directly

Dario Amodei, CEO of Anthropic, has made multiple public statements through 2024-2026 predicting that AI will eliminate a substantial share of entry-level white-collar work over a relatively short time horizon. The most widely-cited version of his prediction: "AI could eliminate 50% of all entry-level white-collar jobs within the next five years, potentially pushing U.S. unemployment rates to 10-20%." He has used the phrase "white-collar bloodbath" to characterize the potential scale. He has said publicly that most affected workers "don't believe it" and that "it sounds crazy" — but that the structural reality is approaching faster than the popular discussion has acknowledged.

The framework's analytical engagement with Amodei's claim requires distinguishing several layers carefully.

At the structural level, Amodei is identifying a real phenomenon. The substitutability of large language model output for many categories of entry-level knowledge work — drafting routine correspondence, summarizing documents, performing first-pass research synthesis, generating standardized analytical reports, writing routine code, handling structured customer service interactions — is no longer theoretical. The capability exists, has been deployed at production scale by tens of thousands of companies, and is generating measurable productivity improvements that those companies are translating into reduced headcount in the affected functions. The 2025-2026 layoff data is the operational evidence. The framework reads Amodei's structural claim as substantially correct.

At the magnitude level, his "50% within five years" specific figure is more speculative. Predicting employment trajectories at five-year horizons is structurally difficult. The composition of "entry-level white-collar" work is itself shifting as the AI substitution dynamic plays out — what counts as entry-level work in 2030 will not be the same set of tasks that counted as entry-level in 2024. Counter-trends (new categories of work emerging from AI itself, regulatory responses, market saturation effects, productivity gains being reinvested in other functions) can soften or accelerate the trajectory in ways the simple substitution model cannot capture. The framework reads the 50%/5-year figure as a defensible upper bound on plausible scenarios rather than a central forecast.

At the unemployment-rate level, the 10-20% claim is substantially more uncertain. The aggregate unemployment rate is determined by labor force participation, sectoral substitution patterns, geographic mobility, training program scale, demographic factors, immigration policy, and several other variables that operate in ways the AI substitution dynamic alone cannot determine. Goldman Sachs economist Pierfrancesco Mei published research in May 2026 estimating that AI-driven displacement could add "up to an additional 0.3 percentage points to the unemployment rate in 2026" — substantially smaller than Amodei's implied range, though Goldman acknowledged the risks were skewed toward larger effects. The framework reads the most likely 2026-2028 trajectory as unemployment drifting from 4.3% toward 5-6% by year-end 2027, with the composition of unemployment shifting more dramatically than the headline number — exactly the dynamic visible in the April 2026 data.

At the political-economy level, Amodei's framing as "bloodbath" is rhetorically loaded in ways the framework needs to engage carefully. A 50% reduction in entry-level white-collar headcount over five years would produce real economic dislocation, but it would not be unique in U.S. labor market history. The manufacturing sector experienced comparable percentage reductions over roughly comparable timeframes during the 1979-1990 period. Agriculture experienced even more dramatic percentage reductions over the longer 1900-2000 period. The framework's broader observation: labor markets have absorbed structural transformations of this magnitude before, with substantial individual hardship during the transitions and substantial aggregate adjustment over longer horizons. The 2026 AI dynamic is genuinely new in its specific mechanisms but is not unprecedented in its structural form. Households navigating the transition face real and difficult adjustments; the broader economy is likely to absorb the shock over a longer time frame than the most dramatic predictions suggest.

The framework's specific reading of Amodei's claim, summarized: the structural phenomenon he identifies is real; the specific magnitude is at the upper end of plausible scenarios; the political-economy framing as catastrophe is rhetorically stronger than the data currently supports but is not unreasonable as a worst-case attention-forcing position. The most consequential thing about Amodei's statement is not whether his specific numbers prove correct. It is that the CEO of one of the leading AI laboratories is publicly acknowledging structural labor displacement at a scale that, if even partially correct, requires fundamental reconsideration of how the U.S. labor market and its supporting institutions function. The framework's analytical job is to engage that reconsideration rigorously rather than waiting for the data to confirm whichever specific magnitude Amodei used in any particular interview.

Menger's saleability criteria applied to labor

Carl Menger's 1892 essay On the Origin of Money identified the saleability spectrum as the structural mechanism by which different commodities sort into more-monetary and less-monetary roles in market exchange. The six criteria Menger identified — divisibility, durability, transportability, homogeneity, widespread demand, and freedom from political weaponization — were developed for physical commodities but apply with surprising precision to labor itself when labor is treated as the asset class workers are selling into the market.

Divisibility. Labor hours can be sold at different granularities: full-time positions, part-time positions, gig work, project-based contracts, hourly billing, milestone-based compensation. The 21st-century labor market has substantially expanded the available granularities through gig platforms (Uber, DoorDash, Upwork, Fiverr) and the broader contractor economy. The framework's reading: labor's divisibility has increased over the past two decades, with substantial benefits for some workers (flexibility, multiple income streams) and substantial costs for others (loss of benefits, irregular income, reduced bargaining power). The 2026 AI substitution dynamic interacts with divisibility in specific ways — AI is most readily substituting work that can be specified as discrete, deliverable, evaluable units (the same kind of work that gig platforms have been disaggregating into discrete tasks for years).

Durability. Skills depreciate at different rates, and the depreciation rate is one of the most consequential variables in 2026 labor saleability. Physical trade skills — electrical work, plumbing, HVAC, welding, carpentry — depreciate slowly because the underlying physical reality the skills address (buildings, infrastructure, equipment) changes slowly. A master electrician trained in 2000 retains substantial value in 2026; the National Electrical Code has evolved but the core skill set transfers. Programming skills depreciate much faster: a 2000-trained Java developer who did not continuously update their skills would be substantially obsolete in 2026; an LLM-assisted developer in 2026 might be obsoleted by 2030 as the AI capabilities continue to evolve. The framework's reading: labor's durability is now sharply heterogeneous across skill categories in ways that the conventional "labor market" framing flattens.

Transportability. Labor's geographic transportability has historically been one of its key constraints. Physical work requires the worker to be physically present at the work site; this is what locks in geographic wage differentials, drives the high pay of skilled trades in specific markets (data-center electricians in Northern Virginia, oilfield workers in the Permian), and limits cross-border substitution. Digital knowledge work has been substantially more geographically portable for decades, which is why it was the work most exposed to offshoring through the 2000s-2010s and is now the work most exposed to AI substitution. The framework's reading: labor that is geographically constrained is substantially protected from AI substitution by the same mechanism that historically protected it from offshoring. The data-center electrician earning $280,000 in Northern Virginia is not in competition with electricians in Bangalore (geographic constraint); they are also not in competition with AI (physical work the AI cannot perform).

Homogeneity. A homogeneous good is one where one unit is functionally equivalent to another. Labor has historically been heterogeneous — individual workers bring different skills, productivity, reliability, and judgment to ostensibly similar roles. AI substitution is now operating particularly strongly on work that is more homogeneous — routine document drafting, basic customer service, standardized analysis, structured code generation — where the variation between workers in the same role is small relative to the variation that AI versus human performance produces. The framework's reading: labor whose performance is highly variable between workers (skilled trades, complex professional services, creative work with genuine artistic judgment) is more saleability-protected than labor whose performance is relatively homogeneous across workers. The AI substitution dynamic is, paradoxically, increasing the saleability premium on labor that is genuinely differentiated.

Widespread demand. Demand for labor categories is shifting in ways visible in the 2026 data. Demand for entry-level programming work is contracting (software development job posts down 8.5% year-over-year in early 2025; the trend has accelerated in 2026). Demand for skilled trades is expanding (electricians projected 9% growth, well above the 3% average for all occupations; HVAC 8%; data center construction driving electrician demand to historic highs). Healthcare demand is structurally increasing as the population ages. The framework's reading: demand-side saleability is following the same pattern as the supply-side analysis — AI-substitutable work is losing demand-side support; physical and care work is gaining it.

Freedom from political weaponization. Menger's original sixth criterion concerned the susceptibility of a monetary commodity to state seizure or restriction. The 2026 application to labor requires extending the criterion to include quasi-political weaponization through corporate substitution decisions. When a major corporation decides to substitute AI for entry-level analyst work, the affected workers face an extraction operation structurally analogous to (though legally distinct from) the kind of seizure that the Mengerian framework historically identified at the state level. The HBR finding from February 2026 — that companies are "laying off workers because of AI's potential, not its performance" — captures this dimension precisely: some portion of the 2026 AI-attributed layoffs reflects actual capability-driven substitution; another portion reflects corporate decisions to use the AI narrative as cover for cost-cutting that would have happened regardless. Either way, the affected worker experiences the same outcome: their labor's saleability has been impaired by decisions they did not participate in and cannot meaningfully resist.

The composite reading across the six criteria: labor in 2026 is exhibiting heterogeneous saleability profiles that vary by an order of magnitude across occupational categories, with the divergence accelerating rather than narrowing. The conventional "labor market" is the aggregate of dramatically different saleability trajectories operating simultaneously.

The specific inversion, decomposed

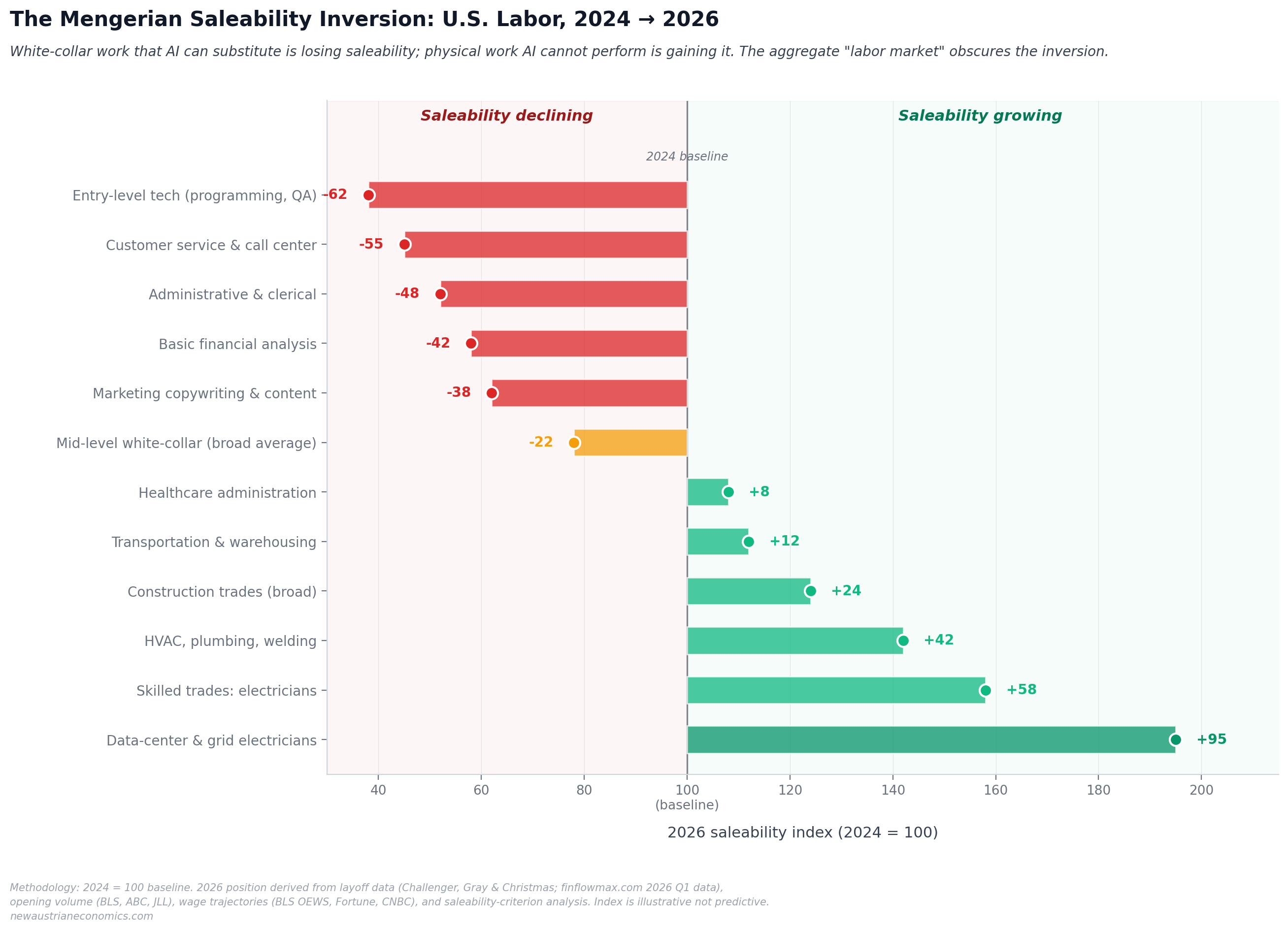

The chart above visualizes the framework's saleability decomposition across twelve U.S. occupation categories. The methodology combines layoff data (Challenger, Gray & Christmas reports, Bureau of Labor Statistics releases), opening volume estimates (Associated Builders and Contractors, JLL skilled trades research), and wage trajectory information (BLS Occupational Employment and Wage Statistics, Fortune, CNBC reporting) into a single illustrative saleability index normalized to 2024 = 100.

The decomposition produces several specific observations worth examining.

Entry-level tech work has lost approximately 60% of its 2024 saleability by 2026. This is the steepest decline in any category and reflects the most direct AI substitution dynamic. Software development job postings declined 8.5% year-over-year through early 2025, with the decline accelerating through 2026. Companies are reducing headcount in the affected functions while reporting productivity improvements from AI tools. The 9,200 Q1 2026 tech layoffs explicitly attributed to AI represent the visible portion; the larger pattern of attrition and reduced hiring extends substantially beyond formal layoff announcements.

Customer service, administrative, basic financial analysis, and marketing copywriting have lost 40-55% of 2024 saleability. These categories share a common structural feature: the work product is highly homogeneous, the task can be specified as discrete deliverables, and AI substitution produces output that is comparable in quality to median human performance at substantially lower cost. The framework's reading: these categories will likely continue to contract through 2027-2028 as the AI deployment cycle works through the affected employer base.

Mid-level white-collar work has lost approximately 20% of 2024 saleability. The smaller decline reflects the structural reality that mid-level work typically involves judgment, coordination, and accountability dimensions that AI does not yet substantively replicate. The HBR research suggests that mid-level managers retain meaningful value as supervisors of AI-augmented teams, but the team sizes they supervise are shrinking. The framework's prediction: mid-level work will face further saleability erosion through 2027-2030 as AI capabilities extend further up the cognitive complexity ladder.

Healthcare administration, transportation, and warehousing have gained 8-12% saleability. These categories are gaining because demand-side factors (aging population, e-commerce growth, supply chain reconfiguration) are operating independently of AI substitution dynamics. The work involves physical presence, regulatory compliance, and human-judgment dimensions that AI cannot easily replicate.

Construction trades broadly have gained 24% saleability. The specific subcategories within trades have gained more: HVAC, plumbing, and welding at +42%; skilled electricians at +58%; data-center and grid electricians at +95%. The acceleration toward the trades reflects both the demand-side pressure from infrastructure investment and AI data center construction, and the supply-side constraint from the demographic structure of the existing trades workforce (large cohorts approaching retirement; insufficient pipeline of younger workers entering the trades).

The composite picture: 2026 labor saleability is bifurcating sharply, with the divergence concentrated along the AI-substitutability axis. Work that AI can perform is losing saleability faster than at any point in postwar U.S. labor history; work that requires physical presence, embodied judgment, or human relationship is gaining saleability at corresponding rates. The aggregate unemployment figure (4.3% in April 2026) is the average across these dramatically different saleability trajectories. It conceals more than it reveals.

The Cantillon distributional dimension

Richard Cantillon, writing in approximately 1730, identified a structural observation about monetary expansion that has become central to the Austrian economic tradition: new money does not enter the economy uniformly. It enters at specific points — historically through sovereign spending, mining operations, banking expansions — and propagates outward from those entry points through specific transmission mechanisms. The agents nearest the injection point benefit first, often substantially, while the agents farthest from the injection point experience the inflationary consequences without the corresponding benefit. The Cantillon Effect, as it came to be called, is the framework's primary diagnostic tool for understanding how monetary expansion redistributes wealth as well as raising aggregate price levels.

The 2026 AI substitution dynamic is operating with structural similarity to the Cantillon Effect, but in the labor dimension rather than the monetary dimension. The AI capability is being injected at specific points in the economy — the companies that deploy it most aggressively, the workers whose roles are augmented rather than substituted, the capital holders whose AI investments produce returns. The propagation outward from those injection points produces sharply differentiated outcomes across the labor force, with the workers nearest the AI deployment point benefiting (productivity gains, augmented capabilities, higher compensation) and the workers farthest from it experiencing the displacement consequences without the corresponding benefit.

The framework's specific observation: the AI substitution dynamic is producing a labor-market Cantillon Effect of substantial magnitude, with the distributional consequences likely to be more economically and politically consequential than the aggregate productivity gains. A 2026 software engineer at a top-tier AI company, working with state-of-the-art AI tools to amplify their productivity, is operating in the equivalent of the early Cantillon injection point — they capture substantial value from the AI capability before its broader market effects fully arrive. A 2026 entry-level analyst at a mid-tier firm whose role is being eliminated as their employer adopts AI tools is operating in the equivalent of the Cantillon periphery — they bear the displacement consequences without participating in the productivity gains.

The political-economy implication: the aggregate "AI boost to GDP" projections (variously estimated at 1.5%-7% over the 2025-2035 period depending on the specific source) describe the aggregate gain across all economic actors. They do not describe how the gain is distributed. The distributional pattern, as the Cantillon framework predicts, will be sharply unequal, with the gains concentrated in the AI capability suppliers, the AI capability deployers, and the workers whose labor complements rather than substitutes for AI. The losses will be concentrated in the workers whose labor substitutes for AI and the broader economic ecosystems (small towns dependent on call center employment, professional services hubs dependent on entry-level analyst pipelines) that the substituted labor categories supported.

The framework's broader catalog has documented Cantillon-like distributional effects across multiple domains: the post-2008 QE programs (Article 4 on OMO and capital erosion), the housing market's metro-level heterogeneity (Articles 17-19), the precious metals paper-physical decoupling (Article 24), the cryptocurrency seizure mechanisms (Article 25). The labor-market Cantillon Effect from AI substitution is the latest entry in this pattern, and structurally one of the most economically significant because labor income remains the primary source of household economic security for the substantial majority of Americans.

The credential decoupling completes

Article 23 of this catalog engaged the college credential as a low-saleability asset whose underlying value proposition was eroding through the combination of cost inflation, demographic pressure, and AI substitution effects. The argument concluded that the small private college closure wave (48 nonprofit colleges closed since March 2020, affecting 52,000+ students) was the visible institutional manifestation of the credential's underlying saleability compression.

The current essay completes the structural argument that Article 23 began. The college credential is losing saleability because the labor it certifies is itself losing saleability — but the two saleability declines are decoupling from each other in ways that produce specific operational consequences. The mid-tier liberal arts degree historically certified its holder for entry-level white-collar work; that work is the category losing saleability fastest in 2026. The trade certifications and apprenticeship programs that traditionally received less institutional prestige and lower lifetime earnings are now certifying for work whose saleability is rising sharply. The credential hierarchy and the labor saleability hierarchy, which were substantially aligned for most of the postwar period, are now inverting relative to each other.

The Pell Grant program's July 1, 2026 expansion to cover 8-to-15-week vocational programs is a specific institutional acknowledgment of this inversion. For the first time in the program's history, the federal financial aid apparatus that historically subsidized four-year college attendance is now subsidizing short-form vocational training that produces direct entry to trades earning $60,000-$120,000 starting salaries. The corporate training investments ($365 million in pledged commitments by mid-2026 from BlackRock, Lowe's, Google, and others) operate in the same direction.

The framework's reading: the credential-labor decoupling will continue to widen through the late 2020s, with structural consequences for higher education institutions, household financial planning, and broader social hierarchies that depended on the previous alignment. Households making post-secondary education decisions in 2026 face genuinely different choice architecture than households making the same decisions in 2010 — the four-year college option is no longer the dominantly correct choice for most pre-college students whose post-graduation career interests align with categories the AI substitution dynamic is eroding.

What households should take from this

The framework's specific operational observations for household readers:

Career and skill investment decisions should be evaluated against AI-substitutability profiles, not against historical category prestige. A 2026 high school student considering whether to pursue a four-year computer science degree, a two-year electrician apprenticeship, a healthcare technical training program, or a different path entirely is making a decision under fundamentally different conditions than the same decision in 2015. The framework's specific recommendation: weight the saleability trajectory analysis at least as heavily as the absolute compensation comparison. A category with current compensation 30% lower but rising saleability trajectory may outperform a category with current compensation 30% higher but declining trajectory across a 30-year career horizon.

Mid-career professionals in AI-substitutable categories should consider their structural exposure honestly. Workers in entry-level and mid-level white-collar categories whose roles align with the AI substitution dynamic face genuine displacement risk over the next 3-7 years. The framework's recommendation: evaluate whether your current role's structural saleability is being maintained, eroded, or amplified by the AI capabilities your employer is deploying. If your role is being amplified (you supervise or coordinate AI-augmented teams), your saleability is likely improving. If your role is being substituted (your output is comparable to AI output at substantially lower cost), your saleability is declining regardless of your current compensation level.

The AI-proof premium will likely compress over time as supply responds. Current trade premium pricing reflects the temporary supply-demand imbalance from the inflow of demand (data centers, infrastructure, post-pandemic construction backlogs) hitting an outflow of supply (retirement of existing trades workers, decades of underinvestment in the training pipeline). The premium is real and will persist for years, but it will likely compress as supply responds. Workers entering the trades in 2026 should not assume the current $280,000 data-center electrician compensation will persist indefinitely; the framework's prediction is that premium compensation in the trades will moderate toward more historical norms by approximately 2030-2032 as the supply pipeline reaches new equilibrium.

Geographic decisions interact with the labor saleability inversion in specific ways. Metropolitan areas whose economies depend on AI-substitutable knowledge work face different forward trajectories than metros whose economies depend on physical work, healthcare, infrastructure, or skilled trades. The framework's prior metro saleability work (Article 17) identified housing-specific stress patterns; the labor saleability analysis adds a second dimension. Households making relocation decisions in 2026 should evaluate both housing market saleability and labor market saleability for their target metros, recognizing that the two saleability profiles may diverge in ways that complicate the decision.

The closing observation

The Bureau of Labor Statistics will release the May 2026 employment situation report on June 6, 2026, three days before this essay's publication. The release will likely report monthly job growth somewhere in the 100,000-150,000 range, unemployment in the 4.2-4.5% range, and average hourly earnings growth somewhere around 3.5-4.0% year-over-year. The headlines that follow will, predictably, describe the labor market as "resilient" or "moderating" or "stable" depending on which financial press source is doing the describing.

The framework's reading is that none of those characterizations will capture what is actually happening. The labor market is not resilient; it is bifurcating. It is not moderating; it is being restructured. It is not stable; it is undergoing the most significant compositional transformation since the postwar manufacturing-to-services transition that played out across the 1970s-1990s. The aggregate figures the BLS reports are technically accurate within their own definitional structure but substantially fail to capture the divergence that is the actual story.

The framework's broader catalog has consistently argued that aggregates obscure more than they reveal in 2026, and that the structural transformations underway across multiple sectors are visible to the careful analyst who decomposes the aggregates into their saleability-relevant components. The labor market is the latest sector to demonstrate this pattern. The 4.3% unemployment rate is the average across labor saleability trajectories that range from -62% (entry-level tech) to +95% (data-center electricians). The "average" worker in that aggregate does not exist in any meaningful sense; the aggregate is the statistical mean of a distribution whose variance is rising faster than its mean is changing.

The framework's analytical job, throughout this catalog, has been to make the structural reality visible while the aggregates continue to report numbers that fail to capture it. The labor saleability inversion is now empirically demonstrable, operationally visible in the 2025-2026 layoff and openings data, and consistent with the broader substrate-fragility thesis the catalog has been documenting. Whether Amodei's specific 50%/5-year projection proves correct, or whether the dynamic proves slower and more manageable than his rhetoric suggests, the structural direction is the same: human labor's saleability spectrum is being reordered along the AI-substitutability axis, and the reordering will produce sharply differentiated outcomes across the workforce that the headline employment figures cannot describe.

The next installment of Watching the Cracks, provisionally Article 29, will engage the May 2026 CPI release scheduled for June 10. The framework's Article 26 made specific predictions about the Hormuz supply shock propagation timeline. The May print is the first major data point that should reflect meaningful Hormuz transmission per the framework's calendar mechanics. Whatever the print shows, the framework will engage it honestly against the prior predictions. The pattern of substrate-fragility validation continues to accumulate. The labor market joins the list of sectors where the catalog's structural reading has now been empirically validated by specific 2026 events.

The aggregates will continue to be reported. The financial press will continue to engage them as if they meaningfully describe what is happening. The framework's contribution remains what it has been throughout this catalog: making the structural reality visible to the household and the analyst who need to navigate it on terms more accurate than the aggregates allow.

This is the twelfth installment of "Watching the Cracks." The framework's predictions recorded here for future testing: unemployment will drift toward 5-6% by year-end 2027, with composition shifting more dramatically than the headline number; trade premium compensation will moderate toward historical norms by 2030-2032 as supply pipeline reaches new equilibrium; AI substitution will continue to accelerate in entry-level white-collar categories through 2027-2028 before reaching diminishing returns as the affected employer base completes the deployment cycle; mid-level white-collar work will face further saleability erosion through 2027-2030 as AI capabilities extend up the cognitive complexity ladder. The saleability inversion chart at the top of this essay shows twelve occupation categories ranked by 2026 saleability versus 2024 baseline, with methodology drawing on Challenger, Gray & Christmas layoff reports, BLS Occupational Employment and Wage Statistics, ABC construction workforce research, JLL skilled trades research, and the framework's six-criterion saleability analysis.

Related essays

The Saleability Audit of Bitcoin: What Menger Would Say in 2026

Bitcoin maximalists insist Bitcoin is the most saleable monetary good ever created. Skeptics insist it doesn't work for the African villager or the rural Chinese citizen the maximalists invoke. Both positions miss what Menger's framework actually says when applied carefully. The audit produces uncomfortable results in both directions — Bitcoin scores remarkably well on some criteria and remarkably poorly on others — and the actual ground-truth of crypto adoption in emerging markets in 2026 is something neither camp accurately describes.

The Decay Function of Marketability: Toward a Computable Menger-Fekete Framework

Menger argued that saleability is a spectrum; Fekete developed the gold basis to measure it for one commodity. This essay proposes a generalizable decay function of marketability, measurable across every modern financial instrument, that renders Menger's core insight computable for the first time.

The Paper Substitute: Agency Mortgage-Backed Securities and the Next Saleability Crisis

Fannie Mae and Freddie Mac issue $9 trillion in paper claims on an asset class — single-family housing — that has the worst saleability characteristics of any major investment available to American households. This is precisely the structure Fekete identified as the most fragile in any monetary system: a deep, liquid market in paper substitutes for an underlying that cannot itself be substituted. The 2008 collapse was the first observable failure of this architecture. The next will be larger.