On April 14, 2026, the Board of Trustees of Hampshire College — a private liberal arts institution in Amherst, Massachusetts, founded in 1965 as an experimental alternative to traditional undergraduate education, alma mater of Ken Burns and Lupita Nyong'o — voted to permanently close the institution at the end of the fall 2026 semester. The school had narrowly avoided closure in 2019 through a last-minute alumni fundraising effort, had attempted a turnaround that included refinancing $21 million of debt and selling off campus land to raise funds, and had seen enrollment recover from a low of 472 students in 2021 to 844 by 2024. The recovery did not hold. Fall 2025 enrollment fell 11.3% to 747 students. The endowment, which stood at $54 million in 2019, has fallen to approximately $24 million. The trustees concluded that no realistic financial path existed to continue operations beyond December 2026.

Nine days later, on April 23, the Board of Trustees of Anna Maria College — an 80-year-old Catholic institution in Paxton, Massachusetts — announced that academic operations would cease at the end of spring 2026. The Massachusetts Department of Higher Education had formally flagged the college as a closure risk less than two weeks earlier. With Anna Maria's announcement, the count of 2026 nonprofit college closures reached eight. Combined with seven closures in 2025 and seventeen in 2024, the post-pandemic total approaches forty-eight institutions closed or announced for closure since March 2020, affecting more than 52,000 students.

The conventional explanations for the closures are well-documented and largely correct as far as they go: declining enrollment, the demographic cliff (the relatively small high-school graduating cohorts now reaching college age, reflecting the post-2008 birth rate decline), competition from larger institutions, regional concentration of supply in the Northeast and Midwest, the structural difficulty of small institutions with high fixed costs and low endowments. Hampshire's NECHE accreditation report identified specific local factors: failure to sell off land assets, inability to restructure debt, overreliance on endowment funds for operations. Each closure has its specific contributing causes. The framework's analytical job is not to dispute any of these factors but to identify what they have in common and what the underlying structural pattern reveals.

This essay is the seventh installment of the Watching the Cracks series. It does three things. First, it walks through the cost trajectory that produced the current situation — forty-six consecutive years of college tuition compounding faster than overall inflation and faster than wages. Second, it applies the framework's saleability analysis to the college degree itself, treating the credential as an asset class whose monetary properties have been systematically degraded by the same trajectory that produced the financial pressure on the institutions issuing it. Third, it engages what artificial intelligence specifically does to the degree's value proposition — not as a future threat, but as a present-tense reality that is already reshaping employer hiring decisions and student return-on-investment calculations.

The framework's reading runs through all three: the credential is, in Menger's terms, a low-saleability asset that has been treated as a high-saleability asset by financial markets, household decision-making frameworks, and institutional planning, for several decades; the gap between the assumed properties and the actual properties has been widening steadily; and the closures now visible in the data are the institutional manifestation of that gap closing.

The cost trajectory

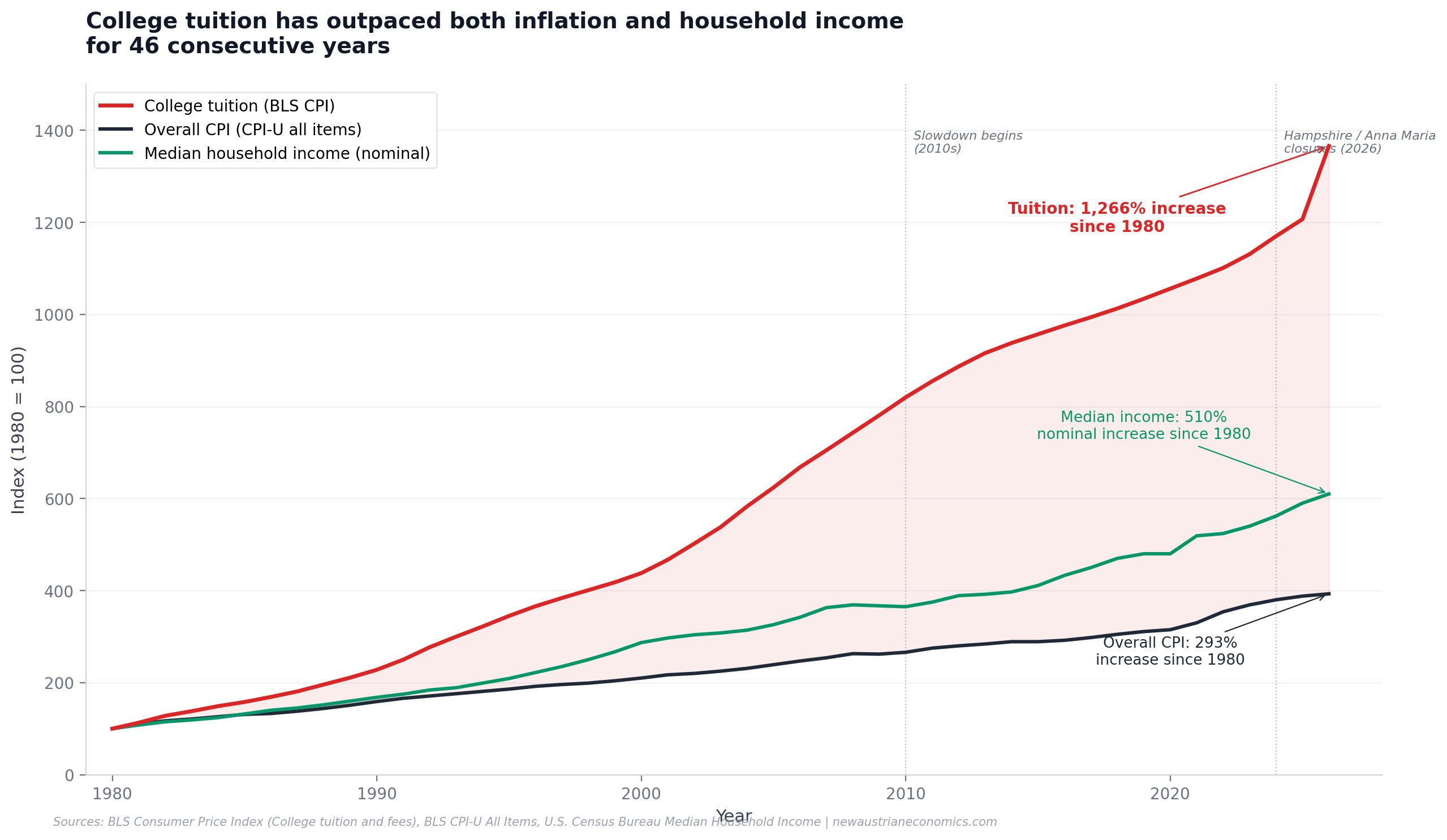

The Bureau of Labor Statistics began tracking the Consumer Price Index for College Tuition and Fees in 1977. The index value at that time was 57.9. The April 2026 index reading was 967.9. The cumulative increase: 1,571% over 49 years, an average annual rate of 5.92%. The corresponding figures for the overall Consumer Price Index across the same period: 3.51% annual average, 408% cumulative increase. Tuition has outpaced overall inflation by approximately 2.4 percentage points per year, every year, for nearly half a century.

The cumulative effect of compounding at a 2.4 percentage point premium for 49 years is visually striking. The chart below presents the trajectory.

The framework's reading of this chart is that what looks like a single phenomenon — "tuition rising faster than inflation" — is actually three distinct dynamics operating simultaneously.

Dynamic 1: Cost-push inflation specific to the higher education sector. Higher education is structurally labor-intensive (faculty salaries, administrative staff, support services) and is not easily susceptible to the productivity improvements that have reduced unit costs in other sectors. Baumol's cost disease — the observation that labor-intensive services that resist automation will see prices rise relative to the broader economy as productivity-driven wage growth in other sectors pulls labor costs up in the unproductive sectors — explains a substantial portion of the cost trajectory. The framework's reading: this is a real factor and accounts for perhaps 1-1.5 percentage points of the 2.4 percentage point premium.

Dynamic 2: Subsidy capture through the federal student loan program. The federal direct loan program has expanded substantially since its original 1965 authorization. By 2024, outstanding federal student loan debt had reached approximately $1.6 trillion, with average debt-at-graduation of $38,792. The framework's reading is that the availability of federal lending has functioned as a subsidy whose capture has flowed primarily to the institutions rather than to the students. Where a student can borrow more, institutions can charge more, and the loan availability has expanded faster than the underlying value being delivered. This is the Bennett hypothesis (named for William Bennett's 1987 observation), and the framework treats it as an additional 0.5-1.0 percentage points of the trajectory.

Dynamic 3: Signaling-and-credentialing dynamics that reward fixed-position institutional status. Higher education functions partly as a signaling mechanism — the degree conveys information about the holder's prior cognitive performance, work ethic, and ability to complete extended structured tasks. Where a degree from an institution with a higher position in the perceived prestige hierarchy is worth more than a degree from a lower-position institution, the price the higher-position institution can charge is bounded primarily by the marginal applicant's willingness to pay rather than by any cost-of-delivery considerations. The framework reads this as adding perhaps 0.5-1.0 percentage points to the trajectory, but operating particularly at the upper end of the prestige hierarchy.

The three dynamics together account for the full 2.4 percentage point premium. The framework's reading is that all three dynamics operate independently of any genuine improvement in the quality or productivity of higher education delivery. The institutions have not, on average, become more productive at producing graduates with measurably stronger skills or labor-market outcomes. They have become more expensive at producing graduates with approximately the same skills they were producing in 1977.

The chart shows the trajectory beginning to plateau in the early 2010s. This is real and consequential. The 2010s saw the first sustained period in the data series where tuition inflation moderated toward the rate of overall inflation. The 2020s have seen actual declining relative tuition growth, with the April 2026 BLS reading showing 2% annual tuition inflation against 3.8% overall inflation. The framework's reading: the institutions are running into a price ceiling that the market is increasingly unwilling to absorb. The closures are the visible institutional manifestation of that ceiling biting.

The degree as a low-saleability asset

The framework's Article 7 audit of American housing applied Menger's six saleability criteria to identify the structural properties of housing as a monetary asset. The same audit, applied to the college degree, produces analogous results — with several specific observations that the housing case did not produce.

Divisibility. A college degree is fundamentally indivisible. The holder either has it or does not. Partial degrees (transcripts of completed coursework without graduation) have substantially less labor-market value than completed degrees, even where the substantive learning is comparable. The framework reads this as a saleability impairment with no available remediation — unlike housing, where some divisibility is possible (renting out portions, selling fractional interests), the degree as monetary instrument is structurally undivisible.

Durability. Degrees are nominally permanent. Once conferred, they cannot be rescinded except under extreme circumstances (academic fraud, post-graduation discovery of cheating). The framework's reading: degree durability is high in nominal terms but lower than it appears in effective terms. The economic value of a degree depreciates over time relative to newer credentials, current technical skills, and shifting employer preferences. A 1985 bachelor's degree in computer science is technically still the same degree, but its substantive content has been substantially superseded by subsequent developments in the field. The degree's nominal durability masks effective depreciation that the holder cannot easily counteract.

Transportability. Degrees travel reasonably well within the country of origin. International transportability is uneven — the U.S. bachelor's degree is widely recognized in most countries, but the recognition is generally for screening rather than substantive equivalence. Specific professional degrees (medical, legal, engineering) face transportability barriers from regulatory licensure requirements that may require additional certification or examination in the destination jurisdiction. The framework reads this as moderate saleability with structural impediments at international boundaries.

Homogeneity. Degrees are not homogeneous in ways that matter for their monetary function. A bachelor's degree from Harvard and a bachelor's degree from a struggling regional state university are nominally the same credential but command substantially different labor-market values. The non-homogeneity is the central feature, not a secondary characteristic, and it produces a saleability profile that depends heavily on the specific institution rather than on the nominal credential. The framework reads this as a major saleability impairment — a "degree" is not actually a single asset class but a heterogeneous category whose individual members can differ in value by an order of magnitude.

Widespread demand. Demand for college-educated labor has historically been strong and growing. The post-WWII expansion of college enrollment was driven by genuine labor-market demand for the skills that degrees were certifying. The framework's reading is that this demand has been weakening relative to the cost trajectory for at least two decades, with employer surveys consistently showing growing willingness to consider non-degreed candidates for roles that previously required degrees, growth in skills-based hiring frameworks, and explicit policy changes from major employers (Google, IBM, Apple, Bank of America, Accenture) eliminating degree requirements for many positions over the 2020-2024 period.

Freedom from political weaponization. This factor — central to the framework's housing analysis through the eminent domain pattern (Article 22) — operates differently for degrees. Degrees are not directly susceptible to political seizure. They are, however, susceptible to delegitimation through changes in employer hiring preferences, accreditation regime modifications, public discourse about the value of higher education, and shifts in immigration policy that affect international student enrollment. The framework's reading: degrees face a different kind of weaponization risk than housing, operating through legitimacy erosion rather than property seizure, but the underlying saleability impact is structurally similar.

The composite reading of these six criteria, the framework concludes, is that the college degree is and has always been a relatively low-saleability asset that has been treated as a high-saleability asset by the financial structures that have funded it. The federal student loan program treats degree-pursuit as an investment with reliable returns; household financial planning treats the degree as a wealth-building strategy; institutional planning treats demand for degrees as a stable revenue source. All three treatments assume saleability properties the degree does not actually have, and the gap between the assumed and actual properties is the operational mechanism producing the current pressure on institutions.

The demographic and financial pressure

The framework reads the institutional closures as the expected outcome of the saleability compression operating against a specific structural feature of the higher education industry: institutions cannot rapidly scale down. A college with 750 students and the physical plant, faculty, administrative staff, and debt service of an institution sized for 1,200 students cannot simply absorb the gap. The fixed costs continue. The variable revenue (tuition) declines with enrollment. The endowment cannot be drawn down indefinitely without eventually exhausting it. The closures are the terminal phase of this dynamic.

Several specific factors compound the underlying saleability pressure:

The demographic cliff. Nathan Grawe's 2018 book Demographics and the Demand for Higher Education forecast a 15% drop in the number of college-bound 18-year-olds between 2025 and 2029, driven by the post-2008 birth rate decline. The forecast has held with high accuracy. The traditional college-applicant pool is shrinking at the moment when the institutions facing financial pressure most need to maintain enrollment. The Northeast and Midwest, with high concentrations of small colleges and unfavorable demographic trends, are seeing the sharpest pressure. New Hampshire's college enrollment fell 13.6% from 2019 to 2022-2023, outpacing the national average. The SUNY system saw a 20% enrollment decline from 2011 to 2021-2022.

Federal grant funding pressure. Several of the 2026 closing institutions identified specific federal grant losses as contributing factors. Providence Christian, which closed in early 2026, cited the end of its Hispanic-serving institution grant (approximately $600,000 annually) as a critical factor that its $25,322 endowment could not absorb. The framework's reading: federal grant programs have functioned as an implicit subsidy that masked the underlying saleability compression in specific institutional categories, and when the subsidies have shifted or expired, the underlying pressure has become immediately visible.

The closure cascade pattern. Closures produce additional closures through several mechanisms. Affected students who do not complete degree programs (which the SHEEO research shows is the majority of students from closing institutions — only about half reenroll, and only 52.9% of reenrollees complete their degrees) constitute a real cost to the higher-education sector's broader credibility. Faculty and staff displaced from closing institutions enter the labor market under conditions that erode wages at remaining institutions. The institutional capacity of small private colleges as a sector contracts with each closure, reducing the broader sector's lobbying capacity, brand value, and economic significance.

The merger alternative is not always available. Some struggling institutions can merge with larger partners (as several recent cases have done — including Pine Manor College / Boston College, Wheelock College / Boston University, Marlboro College / Emerson). The merger option requires a willing larger partner with strategic interest in absorbing the smaller institution. Many small colleges face the structural reality that no larger institution wants them — their academic programs duplicate larger competitors, their facilities are not geographically valuable, their endowments are too small to be material to the absorbing institution. For those institutions, closure is the only option.

The framework's prediction, recorded here for testing: the 2026 closure count will reach 12-18 institutions by year-end, the 2027 count will likely exceed 20, and the cumulative post-pandemic closure count will surpass 100 institutions by 2030. The most vulnerable categories are small private liberal arts colleges in the Northeast and Midwest, regional public universities in states with declining demographics, and specialized institutions (single-purpose seminaries, niche arts colleges, single-profession technical schools) that lack the program diversity to absorb enrollment pressure.

What AI specifically does to the degree

The framework's broader catalog has engaged AI extensively across the cryptocurrency trilogy (Articles 13, 14, and 15), the AI compute as nascent real bills work (Article 5), and the cryptographic marketability premium analysis (Article 6). The college degree's saleability under AI conditions deserves a specific analytical engagement that the broader catalog has not yet provided.

The conventional discussion of AI's impact on higher education tends to focus on cheating (students using AI to write essays), curriculum (whether universities should teach AI literacy), and labor market displacement (whether AI will eliminate the white-collar jobs that degrees prepare students for). The framework's reading is that these are real but secondary effects. The primary structural effect of AI on the college degree operates through a different mechanism: AI substantively performs many of the cognitive tasks that the degree was supposed to certify the holder could perform, with comparable or superior quality, at substantially lower cost.

This is not a future projection. It is a present-tense reality, observable in 2026. The cognitive tasks that have historically constituted the substantive justification for the four-year college degree — extended written analysis, structured argument, research synthesis, quantitative reasoning, contextual interpretation, comparative evaluation, professional communication — can now be performed by AI systems at quality levels that match or exceed the median college graduate. The framework's claim is not that AI matches the best college graduates at these tasks; it is that AI matches the typical college graduate at substantially lower cost.

The labor-market implications are direct. The employer who has historically hired college graduates for tasks that AI can now perform faces a clear decision: continue hiring college graduates for those tasks at the prevailing wage; or restructure the role to use AI for the substantive cognitive work and hire either fewer human workers or workers without traditional degrees to handle the supervisory and coordination functions that AI cannot yet perform. Across 2024-2026, major employers have been visibly making the second choice. Google, IBM, Apple, Bank of America, Accenture, and dozens of other large employers have eliminated degree requirements for many positions during this period. The framework reads this not as a temporary HR experiment but as a structural recalibration of the degree's labor-market value.

The framework's specific analytical observation: the degree's labor-market value has historically been a composite of three components — signaling (the degree certifies the holder completed extended structured tasks), human capital (the degree imparts specific knowledge and skills), and network access (the degree connects the holder to peer and alumni networks). AI substantively erodes the second component (human capital) while leaving the first and third components intact. The signaling and network functions are not directly replaceable by AI. The substantive knowledge transfer is.

The structural consequence is that the degree's value compresses toward the signaling-and-network component, while the cost continues to reflect the substantive-content component that AI has eroded. This is a saleability impairment in the most direct Mengerian sense — the asset's exchange properties have been altered in ways that the conventional valuation framework does not capture, and the impairment compounds with each additional improvement in AI capability.

A specific household-decision implication follows. A high school graduate choosing in 2026 between four years of college at a typical net cost of $40,000-$60,000 per year (after financial aid) versus alternative paths (trade certifications, direct workforce entry, online learning, apprenticeship programs) is making a different decision than the same graduate would have made in 2010. The framework does not advise the graduate against college. The framework observes that the return-on-investment calculation has shifted in ways that the conventional college-decision frameworks have not yet incorporated, and the affected institutions are seeing the result in their enrollment data before the broader public discussion has caught up to the underlying dynamic.

What households should take from this

The framework's specific operational observations for household readers making higher education decisions in 2026:

The cost trajectory has plateaued, but the value trajectory has weakened more. The relevant comparison is not "is tuition still rising fast?" (it isn't, much) but "is the degree still delivering proportional value?" (it isn't, increasingly). Households evaluating college decisions should compare current degree-cost trajectories against current degree-value trajectories, with attention to specific labor-market outcomes for graduates from comparable institutions.

Institutional category matters more than it traditionally did. A degree from a top-quintile institution (in terms of selectivity, endowment per student, alumni network, and graduation outcomes) retains substantially more saleability than a degree from a middle- or lower-quintile institution. The premium on institutional category has been widening for two decades and is likely to continue widening. The framework's reading: households making degree-pursuit decisions should weight institutional category heavily in their selection, even at the cost of higher tuition or lower-prestige acceptance options.

Field of study is a primary saleability variable. Some fields face heavier AI substitution pressure than others. The framework reads computer science, software engineering, and quantitative analysis as facing high substitution exposure; healthcare, skilled trades, regulated professions (law, medicine, accounting), and roles requiring physical presence as facing lower substitution exposure. Households making field-of-study decisions in 2026 are making a different decision than they would have been making in 2010, with substantially more variation in expected lifetime returns across fields.

The alternative paths have matured. Trade certifications, online learning credentials (Coursera, Google Career Certificates, AWS certifications, individual industry credentials), and skills-based hiring frameworks have improved meaningfully over the past five years. These were not realistic alternatives to the four-year degree in 2010; they are realistic alternatives in 2026 for many specific career paths. The household evaluating the college decision should compare the four-year degree against these specific alternatives, not against the abstract "no degree" option that the conventional college-decision framework typically uses.

The institutional closure risk should factor into specific decisions. A student considering a small private liberal arts college in the Northeast or Midwest should evaluate the institution's financial position before committing. NECHE accreditation reports, the institution's Form 990 filings, recent endowment trajectories, and enrollment trends are publicly available data. The risk of mid-degree closure — with the SHEEO data showing only 47% reenrollment and 52.9% non-completion among those who reenroll — is real and should be priced into the institutional selection decision.

The structural reading

The framework's broader claim from the previous twenty-two essays of this catalog has consistently been that aggregates that appear stable are masking substrate deterioration, and that the substrate deterioration becomes visible only when specific institutional examples reach the point of failure. The college closure pattern is a clean example of this dynamic.

The aggregate has been stable for decades. The number of nonprofit four-year colleges in the United States has hovered between 2,500 and 2,700 across the post-WWII period. The aggregate enrollment has grown. The aggregate financial sector serving the institutions (federal loans, alumni giving, state appropriations) has continued to operate. From the standpoint of any aggregate indicator, the higher education sector has appeared stable through 2024.

The substrate has been deteriorating throughout. Tuition has compounded faster than household income for forty-six consecutive years. The implicit financial premise — that the degree's labor-market value would continue to justify the rising cost — has been weakening for at least two decades. The AI substitution pressure has been building for at least three years and has reached operational scale across 2025-2026. The demographic cliff has been forecast since 2018 and is now arriving on schedule.

The closures are the substrate deterioration becoming visible in specific institutional cases. Hampshire, Anna Maria, Providence Christian, Sterling, Lourdes — each closure tells a specific story about a specific institution. The framework's reading is that the specific stories are the surface; the underlying pattern is the saleability compression of the credential they have collectively been issuing. The compression has been operating for decades; the institutional consequences are now visible.

The framework's final structural observation: the institutions closing in 2024-2026 are the ones with the smallest endowment cushions and the highest tuition dependence; the more financially robust institutions will follow on a delayed timeline. The 2030s will likely see closures among institutions that currently appear secure — mid-tier private universities with endowments in the $100M-$500M range, regional public universities facing state funding pressure, and specialized institutions whose enrollment depends on specific labor markets that AI is disrupting. The current closure wave is the leading edge of a longer transformation; the framework predicts that the wave will continue through the end of the current decade and into the 2030s.

The aggregate measure of "how many colleges are there?" has been a stable number for sixty years. The framework's reading is that this aggregate is structurally less stable than its history suggests, and the next decade will see a meaningful contraction in the total number of degree-granting four-year institutions. The contraction is the institutional manifestation of the saleability compression that the credential has been undergoing throughout. The framework's catalog has documented similar saleability-compression patterns in housing (Articles 7, 17, 18, and 19), banking (Article 16), and the broader monetary substrate (Articles 8 and 12). The college case is the same pattern operating in a different sector.

The next installment of Watching the Cracks will likely return to one of the previously-established threads — the Q1 2026 FDIC Quarterly Banking Profile when the data is fully available, the next round of metro saleability map updates, or a follow-up on the eminent domain pattern documented in Article 22. The watching continues. The pattern is now visible across enough sectors that the framework's structural reading no longer requires defense; it requires only application.

This is the seventh installment of "Watching the Cracks." The framework's predictions recorded here for future testing: 2026 closure count will reach 12-18 institutions by year-end; 2027 count will likely exceed 20; cumulative post-pandemic closure count will surpass 100 institutions by 2030; closures in the 2030s will extend to currently-secure institutions in the $100M-$500M endowment range. The tuition cost chart at the top of this essay shows BLS CPI for college tuition (red) against overall CPI (black) and median household income (green), 1980-2026, indexed to 1980 = 100.

Related essays

The Saleability Audit of Bitcoin: What Menger Would Say in 2026

Bitcoin maximalists insist Bitcoin is the most saleable monetary good ever created. Skeptics insist it doesn't work for the African villager or the rural Chinese citizen the maximalists invoke. Both positions miss what Menger's framework actually says when applied carefully. The audit produces uncomfortable results in both directions — Bitcoin scores remarkably well on some criteria and remarkably poorly on others — and the actual ground-truth of crypto adoption in emerging markets in 2026 is something neither camp accurately describes.

The Decay Function of Marketability: Toward a Computable Menger-Fekete Framework

Menger argued that saleability is a spectrum; Fekete developed the gold basis to measure it for one commodity. This essay proposes a generalizable decay function of marketability, measurable across every modern financial instrument, that renders Menger's core insight computable for the first time.

The Paper Substitute: Agency Mortgage-Backed Securities and the Next Saleability Crisis

Fannie Mae and Freddie Mac issue $9 trillion in paper claims on an asset class — single-family housing — that has the worst saleability characteristics of any major investment available to American households. This is precisely the structure Fekete identified as the most fragile in any monetary system: a deep, liquid market in paper substitutes for an underlying that cannot itself be substituted. The 2008 collapse was the first observable failure of this architecture. The next will be larger.